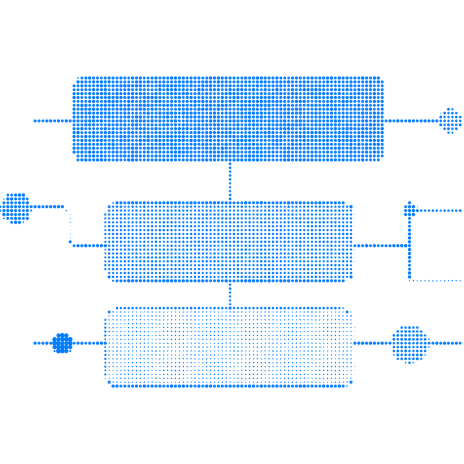

Seven Layers of

Defense-in-Depth

Traditional collections rely on sampled QA after the fact.

This model prevents violations before they occur.

01

Before

Interaction

Interaction

- Policy encoding with Risk/Compliance sign-off

- Strategy boundaries and settlement caps enforced

- Version baseline locked before release

Compliance is structural, not dependent on retraining.

02

During

Interaction

Interaction

- Deterministic guardrails block prohibited language

- Real-time escalation for sensitive scenarios

- Full interaction capture

No off-script moments.

03

After

Interaction

Interaction

- Audit-ready replay by account, cohort, and rule

- Version and change logs for every release

- Continuous drift monitoring

Examiner-ready evidence, not reconstructed explanations.