Debt collection compliance is often treated as legal hygiene, something you train on and document for audits. That works at low volume, but it fails at scale. In reality, debt collection laws and regulations function as operating constraints. They shape recovery predictability, liquidation curves, and class-action exposure long before risk becomes visible.

We have seen portfolios governed by the same debt collection regulations perform very differently under pressure. The statute did not change. The enforcement architecture did, especially across channels, and evolving state debt collection laws.

At a small scale, compliance feels procedural. At volume, it becomes infrastructural.

Timing windows, consent controls, and frequency caps under CFPB Regulation F and the Reg F 7-in-7 rule must be validated before execution. What determines outcomes under modern debt collection laws and regulations is whether those rules are enforced consistently under the law.

What Are the Federal Debt Collection Laws?

At the federal level, debt collection laws and regulations establish the baseline conduct rules for collection activity in the United States.

In practical terms, federal debt collection laws and regulations address several core areas of conduct and accountability.

They govern when and how a consumer may be contacted, what must be disclosed during that interaction, and how frequency limits apply. They also define consumer rights, dispute and validation procedures, documentation standards, and credit reporting obligations.

Key Federal Laws Governing Debt Collection

Fair Debt Collection Practices Act (FDCPA)

The Fair Debt Collection Practices Act (FDCPA) is the federal baseline for third-party activity under U.S. debt collection laws and regulations.

Basically, the statute prohibits:

- Harassment or abusive conduct

- False, misleading, or deceptive representations

- Unfair practices in the collection process

It also regulates:

- When and how consumers may be contacted

- Communication frequency and workplace outreach

- Required disclosures, including the validation notice and “mini-Miranda.”

Violations carry statutory damages of up to $1,000 per action, plus attorney’s fees. In class actions, exposure scales quickly.

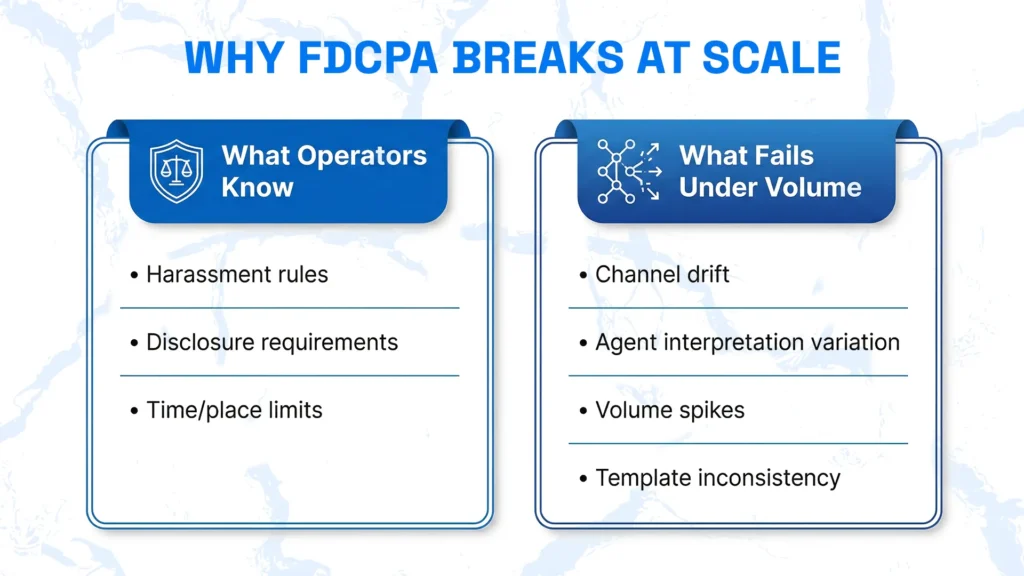

Real-world execution introduces variables that static rules cannot anticipate.

In our experience, the majority of exposure stems from variability. One contact appears compliant in isolation.

But when calls, emails, and voicemails stack within a short window, sequencing exceeds acceptable boundaries under modern debt collection regulations.

Small deviations eventually compound into systemic failures:

- Tone tightens under performance pressure

- Disclosures get shortened

- Cross-channel activity isn’t reconciled in real time

Each action may sit inside the perimeter of the debt collection rules and regulations. The account may not.

Viewed correctly, FDCPA risk is economic.

Systemic variability degrades yield, complicates re-forecasting, and introduces class-action tail exposure that directly impacts portfolio valuation.

The market rewards the reliability of execution over the purity of intent.

Telephone Consumer Protection Act (TCPA)

If the FDCPA defines conduct boundaries under U.S. debt collection laws and regulations, the Telephone Consumer Protection Act (TCPA) defines financial acceleration risk.

The structural difference is:

- FDCPA penalties are typically assessed per action.

- TCPA penalties are assessed per call or per message.

And this distinction is significant.

A single configuration error in an automated campaign can generate thousands of violations in days. For high-volume portfolios, TCPA debt collection exposure compounds faster than most other debt collection regulations risks.

Besides, the evidence trail is unusually clean.

That traceability strengthens aggregation in litigation and makes dispute defense harder once violations occur. Under modern debt collection laws and regulations, documentation cuts both ways.

Recent reporting shows 507 TCPA class actions filed in Q1 2025 alone, more than double the same period the prior year. That escalation reinforces how small consent failures aggregate quickly under modern debt collection laws and regulations.

Implementation adds another layer of complexity:

- Autodialer interpretations vary across institutions

- SMS consent integrity depends on reassignment tracking

- Opt-outs must propagate across systems in real time

- Vendor dependencies introduce hidden coordination risk

At scale, protection comes from deterministic consent validation embedded into execution systems. That is what stabilizes debt collection compliance under TCPA pressure.

CFPB Regulation F

When CFPB Regulation F took effect, many teams treated it as a documentation update. In reality, it was an execution stress test for modern debt collection laws and regulations.

The most visible example is the Reg F 7-in-7 rule.

On paper:

Seven attempts in seven days.

In practice:

Seven is a ceiling, not a quota.

From what we have observed, the first mistake operators make is treating 7-in-7 as permitted activity rather than maximum tolerable exposure.

Sophisticated portfolios often configure tighter limits, such as 3-in-7, depending on risk tolerance and recovery economics. These ceilings are embedded within a broader debt collection rules and regulations strategy.

The real breakdown, however, is structural.

Regulation F applies frequency limits at the account level, not per channel.

That means calls, emails, SMS, and vendor-triggered outreach must be aggregated before enforcement.

Yet most systems were built in silos. One platform logs a call, another triggers a text, and a third sends an email.

Once again, while each system appears compliant under separate debt collection regulations, the account may not be.

Validation notices introduce another fragile layer.

Generating a notice is not the same as proving delivery timing, triggering condition, and channel pathway. Under modern debt collection laws and regulations, proof standards matter as much as behavior.

Account transfers add further risk.

When portfolios move between vendors or internal teams, compliance artifacts are often assumed rather than verified. Regulation F does not accommodate assumption-based enforcement.

This is why operational scale Reg F 7-in-7 rule flaws remain hidden at low volume.

At that point, operational success is a direct function of engineering integrity.

Leading operators are moving toward unified account-level orchestration that aggregates outreach automatically. Manual reconciliation simply cannot sustain debt collection compliance in a Regulation F environment.

FCRA and UDAAP

If statutes like FDCPA and TCPA define specific guardrails within debt collection regulations, FCRA and UDAAP operate differently.

They are not checklist statutes. They are harm-based frameworks.

The Fair Credit Reporting Act (FCRA) governs data accuracy, dispute handling, and credit reporting integrity. UDAAP, enforced by the CFPB, evaluates whether conduct is unfair, deceptive, or abusive, even if no bright-line rule was technically violated.

This is where many programs underestimate risk.

Under UDAAP, a sequence can comply with CFPB Regulation F timing and disclosure requirements and still create exposure.

Why? Because regulators assess the cumulative consumer experience, not isolated steps.

In practice, we’ve seen exposure emerge from:

- Tone escalation across touchpoints

- Sequencing that creates perceived urgency

- Disclosure language that shifts subtly between channels

- Settlement framing that appears coercive at scale

A collection of valid actions cannot mask an indefensible system architecture.

Consistency becomes the control layer. A disclosure present in one channel but absent in another weakens FDCPA compliance posture, even if no single step violates explicit debt collection rules and regulations.

AI adds further interpretive sensitivity. As AI in debt collection becomes more deeply embedded in execution systems, regulators increasingly expect transparency in how outreach decisions are triggered, logged, and documented.

As AI in debt collection expands, regulators increasingly expect transparency and explainability. Explicit identification (“This is a virtual agent…”) is often safer than attempting to simulate human tone. Clear disclosure reduces deception ambiguity and strengthens compliance automation for collections.

FCRA introduces another axis of exposure.

Data integrity. Inaccurate balances, incomplete dispute documentation, or delayed corrections do more than affect recovery. They impact credit profiles. That elevates regulatory sensitivity under state debt collection laws and federal oversight.

The lesson is simple.

UDAAP evaluates systems instead of scripts. FCRA evaluates data integrity and not mere intent.

That scrutiny is reflected in filing data.

Federal court docket data shows FDCPA filings up roughly 36% year-over-year and FCRA filings up approximately 15%, reinforcing that enforcement activity under modern debt collection regulations is accelerating.

How State Law Variability Complicates Debt Collection at Scale

Federal debt collection laws and regulations create the baseline. State debt collection laws are where operational stress begins.

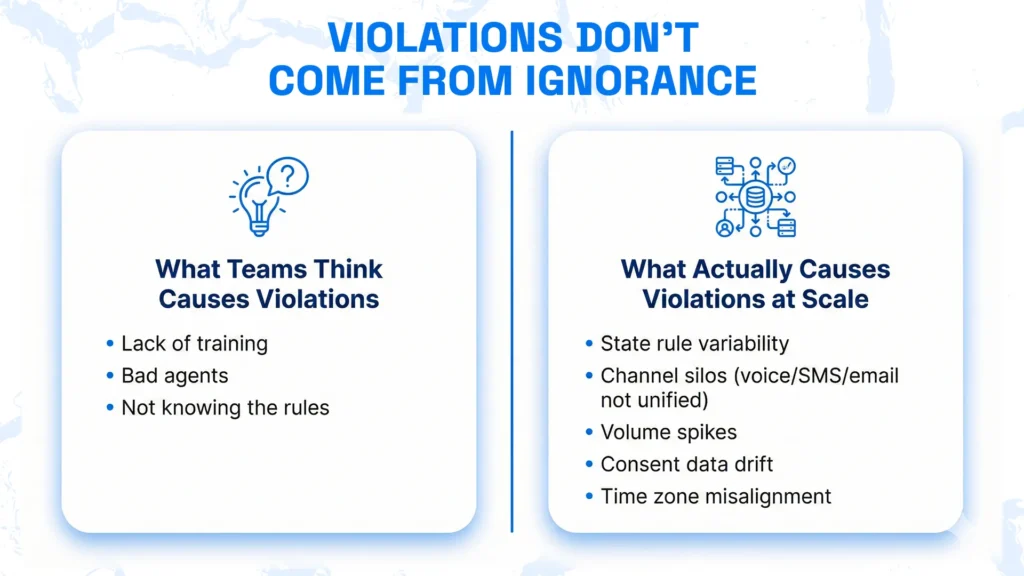

We identify manual ‘ups and downs’ as the leading cause of compliance failure.

At low volume, differences between states feel manageable. Teams rely on guidance memos, quarterly reviews, and occasional rule updates.

That model works until portfolios scale.

States revise their own debt collection regulations independently:

- One updates disclosure language

- Another adjusts call timing windows

- A third changes licensing or consent standards

These evolving rules and regulations for debt collection do not move in coordination. Each update is rational in isolation, but together, they overwhelm manual control systems.

The risk environment is characterized by fragmented, non-simultaneous violations.

Let’s say a campaign launches across ten states. Mid-cycle, one jurisdiction changes its interpretation or effective date. Outreach remains compliant almost everywhere, except for a small slice of accounts.

Nothing in the behavior changed; the system simply failed to adapt fast enough. That is how debt collection violations emerge in practice.

Certain jurisdictions magnify this pressure. California’s Rosenthal Act extends FDCPA-like obligations to original creditors, fundamentally reshaping first-party workflows. New York imposes enhanced disclosure requirements.

For firms handling business receivables, evolving commercial debt collection regulations introduce additional nuance around venue selection, documentation thresholds, and notice timing. These are structural design decisions, not minor configuration tweaks.

Statute of limitations (SOL) differences introduce economic consequences.

SOL variation influences:

- Portfolio pricing

- Recovery projections

- Litigation strategy

- Settlement posture

Models that ignore these differences routinely overstate recoverable value, particularly where overlapping state debt collection laws and federal constraints intersect.

This is where we see organizations make a subtle but costly mistake: treating state requirements as edge cases.

Outliers function as primary parameters within the core logic engine.

When state rules are handled through exception tables and manual overrides, inconsistency accumulates. Forecast variance follows.

Usually, exposure does not stem from ignorance, since teams usually understand the statutes. What fails is enforcement reliability as portfolios grow and regulations evolve.

At scale, manual compliance tracking collapses, especially when federal debt collection laws and regulations intersect with rapidly evolving commercial debt collection regulations across jurisdictions.

Managing complex state rules measures the true strength of an enforcement layer.

Emerging Trends and Recent Developments in Debt Collection Compliance

Modern compliance operates as a system-driven function rather than a policy-driven one. In automated debt collection environments, automation only reduces risk when enforcement logic is embedded upstream rather than layered on after execution.

What we are seeing across the industry is a structural shift.

Enforcement expectations under modern debt collection regulations are no longer satisfied by training decks and updated procedures. Regulators are evaluating how systems behave under load.

Scale is the catalyst.

Scaling across channels requires compliance to be integrated into the system architecture.

Increased Regulatory Focus on Technology-Driven Violations

Regulators now prioritize the audit of technical guardrails over written manuals.

It is no longer enough to show that a rule exists. Institutions must show that systems prevent violations before they occur.

Are frequency caps enforced pre-execution? Does consent validation occur before outreach? Can enforcement logic be demonstrated under stress?

We have noticed that institutions that rely on documentation rather than embedded controls are the ones that struggle under audit.

The deployment of AI naturally invites more granular oversight.

Rising TCPA and Digital Channel Exposure

Digital expansion has widened the exposure surface.

SMS, email, and voice are no longer treated as separate channels. Under TCPA debt collection scrutiny, they are evaluated as a unified contact strategy at the account level.

This shift establishes a new fundamental standard for the industry.

- Frequency limits are aggregated

- Consent histories must be provable

- Opt-out propagation must be real-time

Manual tracking models rarely tend to survive this coordination requirement.

Expanded Scrutiny of Frequency Limits Under Regulation F

Cross-channel enforcement is now assumed.

Institutions that track voice, SMS, and email independently often discover violations only after limits have been exceeded. Compliance requires a live and unified view of all contact attempts across the enterprise.

The 7-in-7 rule serves as a primary design mandate for modern collection engines.

Growing Expectations for Real-Time Auditability

Audit standards are tightening. It is no longer sufficient to show that a notice was generated.

Institutions must demonstrate:

- When the action occurred

- Through which channel

- Under which rule set

- In response to which trigger

Compliance is becoming a data integrity problem.

Fragmented logs and vendor silos now create material enforcement risk.

AI and Automation Moving From Experimentation to Expectation

Automated intelligence represents the new baseline for operational infrastructure, and the future of AI in debt collection is increasingly defined by explainability, replayability, and system-level audit transparency as enforcement scrutiny intensifies.

But with that shift comes new scrutiny. Institutions are expected to explain:

- Why was a message sent

- Why was it sent at that time

- Why that specific language was used in that interaction

Explainability serves as the primary requirement for modern enforcement layers. Enforcement layers must be transparent, replayable, and defensible.

This is where structured compliance automation for collections becomes strategic rather than tactical.

Compliance Moving Upstream Into System Design

The biggest shift we see is upstream integration.

Compliance operates as a native system default within the core architecture.

Organizations that engineer enforcement into execution architecture scale more predictably. Once volume removes room for manual correction, compliance must be embedded.

When that shift happens, something important changes: systemic enforcement decouples risk from volume.

What Are the Most Common Compliance Violations

The primary source of non-compliance is the fragmentation of execution patterns as they scale beyond manual oversight.

Scaling transforms isolated errors into systemic mathematical constants.

Communication Violations

True systemic validity is achieved only through account-level precision.

Communication failures remain the most common FDCPA exposure.

Typical breakdowns include:

- Calls placed outside the 8 am–9 pm window due to inaccurate time zone logic

- Frequency caps degrade when channels operate in silos

- Workplace contact continues because cease requests fail to synchronize

- Detailed voicemails create unintended third-party disclosure

Individually, each system may appear compliant. At the account level, the contact pattern violates the rules.

Disclosure and Representation Violations

Disclosure issues tend to emerge more subtly. They don’t explode overnight. They drift.

Mini-Miranda language gets shortened under performance pressure. Debt balances fall out of sync when payment data doesn’t update in real time. Escalation language appears without documented intent. Tone intensifies across sequences.

At a small scale, these shifts look cosmetic. But under volume, they evolve into repeatable exposure.

Technology-Specific Violations

Digital expansion introduces new failure modes.

- TCPA autodialer risk shifts with evolving interpretation, particularly for AI voice

- SMS campaigns operate on unclear or stale consent histories

- Email workflows misroute account data

- AI calls deploy without explicit disclosure embedded in the flow

Automation amplifies whatever control exists – strong or weak.

Documentation Failures

This is where defensibility collapses.

A validation notice may exist, but delivery timing cannot be proven. Consent artifacts may be present, but fragmented. Call logs may be stored, but missing metadata that ties actions to rules. Dispute handling may occur, but response windows are not demonstrable.

In enforcement settings, documentation is foundational. If it cannot be tied to timestamps and rule logic, it will not withstand scrutiny.

UDAAP-Driven Risk Areas

UDAAP prioritizes consumer outcomes over strict technical conformity. Even when frequency limits and disclosures are satisfied, sequencing, tone, or framing can still trigger exposure.

In practice, risk builds cumulatively.

A/B testing may increase perceived pressure, or tone can escalate across touchpoints. Disclosure language may drift between channels. Settlement offers that are technically compliant can still feel coercive in context.

Regulators perform a holistic assessment of the entire customer journey. That broader lens is where UDAAP risk typically emerges.

How to Build a Compliance-First Collection Process

Reactive compliance measures function as evidence of a failed system.

In our experience, the highest-performing portfolios treat compliance as an architectural constraint.

Treat Compliance as a Portfolio-Level Constraint, Not a Training Problem

Compliance directly impacts yield:

- Violation rates affect liquidation curves

- Forecast variance increases with enforcement drift

- Class-action tail exposure reduces portfolio valuation

FDCPA compliance and broader debt collection compliance are economic variables.

Eliminate Variability Across States, Channels, and Volume Cycles

Most violations are not knowledge failures, but variability failures.

Fifty-plus state rule sets evolve independently. Channel sprawl multiplies enforcement complexity. Volume spikes expose control gaps. Agent interpretation drift compounds over time.

Systemic enforcement provides the physical guardrails that exceed the limits of training.

Shift Compliance Enforcement Upstream Into the Execution Layer

Reactive compliance fails under load.

Enforcement must occur before outreach is triggered. Frequency, timing, consent, and disclosures should be validated pre-execution.

Optimization operates inside fixed constraints.

Control Contact Frequency, Timing, and Channel Access Systemically

Frequency and channel eligibility must be enforced at the account level.

That means:

- Consent and opt-outs propagate across systems

- Time zones are validated automatically

- Channel eligibility is checked before every attempt

Siloed tracking guarantees drift, and this is where structured compliance automation for collections becomes foundational.

Remove Human Discretion From Regulated Actions

Human discretion is essential in negotiation, empathy, and settlement structuring. It is not appropriate to interpret rules and regulations for debt collection.

Timing windows, disclosure triggers, and frequency limits should be system-enforced. The more regulated a step is, the less it should depend on interpretation. Variability decreases when enforcement logic, not memory, governs execution.

Operationalize Special Handling States (Disputes, Cease-and-Desist, Hardship)

Disputes, cease-and-desist, hardship status, and state-specific requirements must alter workflow automatically.

Flags buried in notes fail under volume.

In scaled environments, compliance automation for collections must:

- Restrict cadence

- Block channels

- Modify scripts

- Preserve audit artifacts

Anything dependent on human recall degrades over time.

Use Automation and AI to Enforce Rules, Not Make Decisions

AI in debt collection should function as a constraint engine, not a strategy engine, because the structural differences between AI debt collection and traditional methods become most visible when automation accelerates variability instead of constraining it.

That includes validating timing windows, enforcing frequency ceilings, triggering required disclosures, and generating timestamped audit logs.

The collection strategy remains human. Enforcement becomes deterministic. This separation between strategy and enforcement is what allows operators to apply successful debt collection techniques to maximize recovery rates without increasing compliance exposure.

Maintain Portfolio-Wide Auditability and Defensible Records

Auditability must be architectural.

Every compliance action should produce timestamped, rule-linked evidence. Consent and dispute records must be provable.

Regulators measure success through the technical reliability of your enforcement layer.

Preserve Recovery Predictability While Scaling Volume

When enforcement is deterministic:

- Yield stabilizes

- Forecast variance narrows

- Downside exposure becomes modelable

Compliance acts as the stabilizer that allows for safe yet rapid scaling

Kompato: AI-Powered Compliance Enforcement at Scal

Kompato AI is built as an execution-layer enforcement system designed to eliminate variability before it becomes regulatory exposure. Instead of relying on post-call audits or agent interpretation, it validates compliance constraints pre-execution across voice, SMS, and email. The platform embeds rule enforcement directly into workflow logic, ensuring that outreach cannot proceed unless it meets defined legal parameters. As portfolios expand, compliance stability remains deterministic rather than dependent on manual oversight.

How Kompato AI Handles Scale-Driven Compliance Risk

- 45+ automated compliance checks per interaction

Every outreach attempt is validated for frequency limits, timing windows, consent integrity, and disclosure triggers before execution. This reduces the likelihood that a campaign-level configuration error cascades across thousands of accounts. - 99.9%+ compliance rate with <0.1% flagged interactions

Enforcement logic is designed to minimize drift during volume spikes, seasonal surges, or portfolio onboarding. Flagged interactions are isolated early, preventing systemic exposure. - 100% call recording with 7-year transcript retention

All interactions generate timestamped artifacts linked to rule enforcement logic. This strengthens audit defensibility and aligns with litigation and regulatory documentation timelines. - 10,000+ historical scenario replay tests

Configuration updates are regression-tested against prior interaction scenarios to preserve rule integrity. This reduces the risk that new optimizations unintentionally weaken compliance controls. - Automated rollback within ~15 minutes

If a configuration change degrades performance or enforcement accuracy, the system can revert quickly. This limits downstream exposure and shortens the risk window. - Proven at scale with 100K+ live accounts and millions of calls processed

Compliance controls undergo validation exclusively within live production environments. This demonstrates enforcement stability across high-volume, multi-channel operations.

Final Thoughts: Scaling Without Increasing Compliance Exposure

Scaling debt collection has never been about knowing the law. Most operators already understand the requirements embedded in debt collection laws and regulations. The real constraint is execution. As volume expands across states and channels, small inconsistencies compound into yield volatility, re-forecasting risk, and class-action exposure.

When compliance is treated as policy, exposure grows with scale. When it is treated as infrastructure, outcomes stabilize. Deterministic enforcement, cross-channel consistency, and audit-ready documentation reduce variability at the source. The organizations that scale predictably in 2026 will be those that embed compliance into system architecture, ensuring that volume no longer amplifies risk.

FAQs

Compliance breaks when execution becomes fragmented. Cross-channel drift, timing gaps, and inconsistent enforcement turn known rules into repeatable exposure as volume increases.

TCPA consent failures typically create the greatest financial exposure because penalties multiply per call/message, and the evidence trail supports aggregation at scale. FDCPA and documentation issues still matter, but they usually don’t compound as fast once volume ramps.

Regulators require a high degree of auditability to verify that internal constraints are applied consistently at scale.

Training reduces awareness gaps but cannot eliminate execution variability. At scale, systems, not people, determine whether regulated actions stay within bounds.

Automation amplifies both strengths and weaknesses. Without enforcement guardrails, it accelerates violations; with them, it stabilizes compliance under volume.

What matters is defensible proof: when actions occurred, under which rules, and why. Incomplete or fragmented records are often more damaging than missing actions.