SMS is one of the most effective channels for debt recovery, achieving open rates of 98% and faster responses than calls or mail. It also triggers a complex web of debt collector text message regulations that compliance teams cannot afford to overlook.

For instance, under the FDCPA and CFPB’s Regulation F, SMS messages are treated as “communications” about a debt, and must conform to rules on consent, timing, content, and opt-out mechanisms. Similarly, the TCPA requires prior express consent before an automated SMS can be sent and clear opt-out instructions.

Mishandling debt collector text message regulations can trigger statutory damages, which can be $500–$1,500 per message under TCPA, with class-action litigation posing a significant threat. SMS programs compliant with regulations reduce cost per dollar collected and improve debtor experience.

This guide explores the regulations while guiding on building debt collector text message regulations compliance into SMS workflows so that the rules become an operational advantage.

Why Text Messaging Is Reshaping Debt Collection

The importance of debt collector text messages is driven by operational economics and evolving communication behaviors. Traditional outbound collection is increasingly ineffective as contact rates decline. Spam labeling, call blocking, and mistrust of unknown numbers reduce live answer rates, forcing agents to spend time chasing unresponsive dials instead of engaging consumers.

Meanwhile, SMS and other digital channels consistently deliver higher visibility and engagement, with 44% debt collection agencies utilizing it effectively.

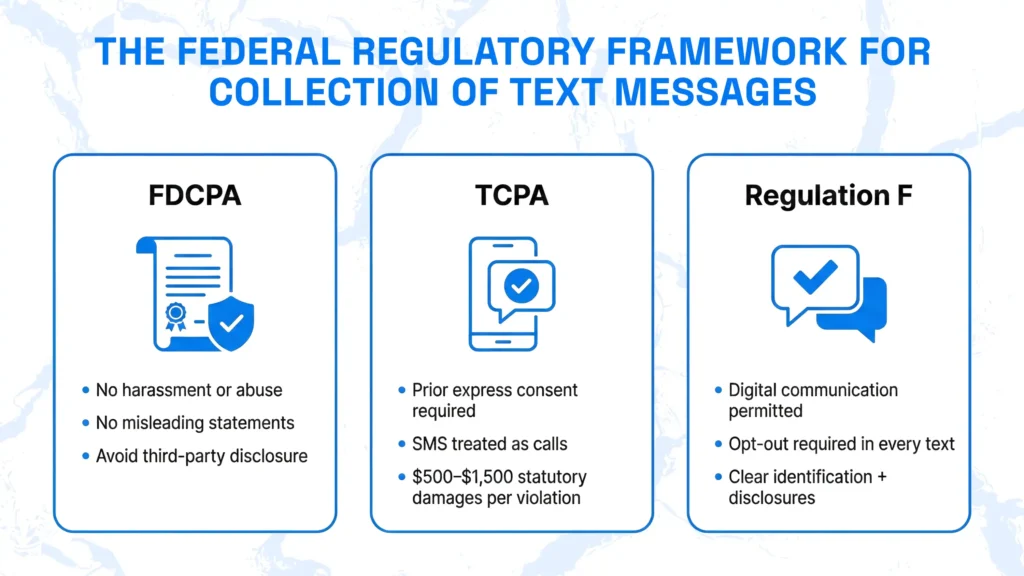

The Federal Regulatory Framework for Collection of Text Messages

Debt collection text messaging is governed by three core federal frameworks that every collection operation must understand before sending a single SMS: the Fair Debt Collection Practices Act (FDCPA), Regulation F, and the CFPB.

Together with overlapping state-specific laws, these are the compliance baseline for any SMS‑based debt collection program.

Fair Debt Collection Practices Act (FDCPA)

The 1977 Fair Debt Collection Practices Act (FDCPA) has been consistently applied to SMS outreach. Under the FDCPA, any communication about a debt, including a text message, must avoid harassment, false or misleading representations, and unfair practices.

For example, repeatedly sending a consumer unsolicited texts, even if they are about unpaid loans, can be considered harassing, oppressive, or abusive conduct that violates the Act, even if the individual message looks compliant. The challenge for debt collection messaging is that SMS can be easily screenshot, forwarded, and produced in litigation, unlike phone calls.

Under the debt collector text message regulations, collectors may not use deceptive tactics and must clearly identify themselves as collectors in communications.

A unique FDCPA risk in texts is third-party disclosure; a message could be seen by anyone with access to the consumer’s phone, and the Act prohibits revealing debt details to third parties. Collectors must also honor cease‑communication requests and avoid unfair timing or excessive frequency, just as with calls or letters.

Telephone Consumer Protection Act (TCPA)

This federal statute sets clear rules for debt collector text messages and the use of automated phone equipment. It limits the use of pre-recorded voice messages, automatic dialing, SMS, and fax.

The TCPA has the most financially punitive debt collection laws. Statutory damages range from $500 per violation in case of negligence and up to $1,500 per violation when done willfully. What is critical for debt collection messaging is that SMS messages are considered “calls” under the statute.

Key concerns here are about express consent to contact a number. Documentation must show that the phone number was provided by the consumer at the time of contract. Risk is elevated with incomplete or poorly documented records.

The success for automated AI messaging tools is that over 70% of consumers give explicit consent for AI communication when asked via a human-first-then-AI-consent workflow.

Regulation F Requirements for Text Messages

The CFPB’s 2021 rule under the Fair Debt Collection Practices Act (FDCPA) modernized federal consumer debt protection laws for digital communications. Regulation F explicitly addresses electronic messages and clarifies that emails and texts are permitted if there are mandatory opt-out mechanisms clearly built in.

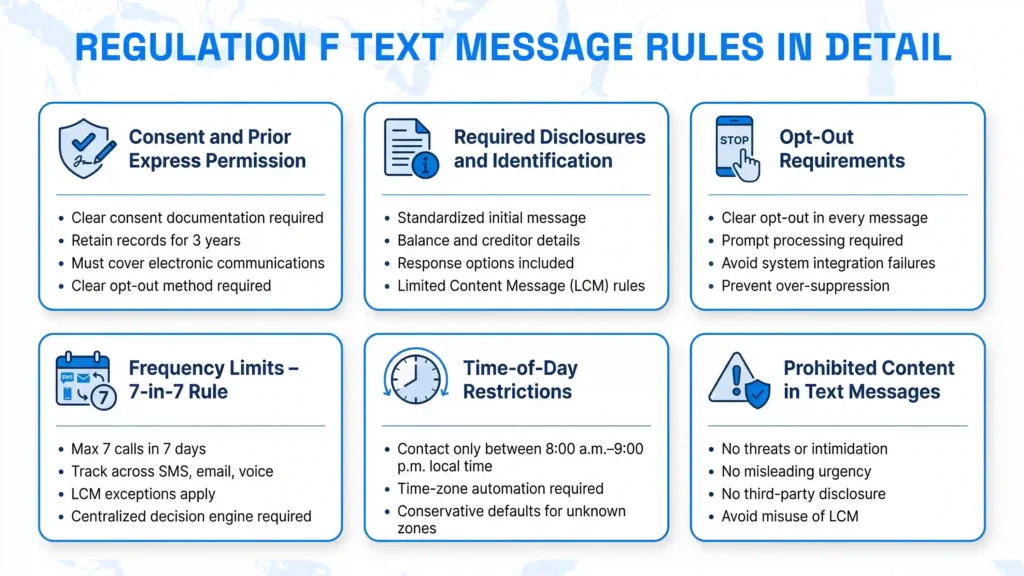

Regulation F Text Message Rules in Detail

Part of the federal consumer debt protection laws, under Regulation F, debt collectors can use emails, text messages, and social media to reach consumers, if they avoid harassment and abusive behavior. The regulation outlines how debt collectors text consumers without sending too many messages or using misleading tactics.

Consent and Prior Express Permission

Currently, Regulation F is the operational blueprint for SMS compliance, and it is treated as an additional layer of regulations over the TCPA rules. To meet debt collector text message regulations, agencies must have clear consent documentation and keep it on record for three years. It should cover electronic communication and have a clear method for the consumer to opt out.

Required Disclosures and Identification

Under Regulation F, the debt collection messaging requirements include using a standardized initial message that clearly lists the key details like balance, creditor information, and available response options.

One beneficial part of debt collection regulations is the limited content message (LCM). This is usually a voicemail left for consumers that must contain required information and could contain other optional information as per federal consumer debt protection laws. An LCM is not classed as a text communication.

A collection text message includes:

- A business name that does not indicate that the caller is a debt collector

- Details of the debt like borrower’s name, purpose, amount outstanding, due date, and payment options.

- Telephone number(s) for getting back to the caller

- A request that receivers reply, and the names of people who can be contacted.

Opt-Out Requirements

Under Regulation F, every debt collector’s text message must include a clear opt-out option. These need to be processed in a reasonable time to enable the consumer to actually “opt out”.

This is a regulatory challenge under debt collector laws. A consumer opts out of receiving debt collector text messages, but the agency systems are not integrated with the SMS platform, and the consumer continues to receive messages.

Another scenario is that the system marks the consumer as no contact when they opt out of a specific medium. This is known as over-suppression. While this does not pose a compliance risk to debt collectors, it reduces revenue because contactable consumers are excluded.

Frequency Limits and the 7-in-7 Rule

As part of the set of federal consumer debt protection laws, Regulation F updates and modernizes them. It is designed to prevent harassment, abuse, or undue pressure on consumers. The base rule of this is the 7 in 7 rule, which limits 7 phone calls in 7 days. This requires collection software that tracks communications across voicemail, and phone calls so that the regulations are not violated.

The exceptions to the 7 in 7 rule include the LCMs discussed earlier and calls that do not get connected. As per debt collection laws, the communication system needs to be thorough enough to track which communications got through and which didn’t.

A centralized decision engine must be in place that tracks communication frequency across all SMS + voice + email against Regulation F limits. Such a system should be flexible enough to include opt-in services, as well as detailed enough to factor in marketing and collection contact efforts.

This is where modern AI debt collection messaging systems like Kompato AI have an edge, as they are comprehensive enough to give a far more detailed compliance picture, and flexible in moving from 7 in 7 to as low as 1 in 7 for more sensitive segments.

Time-of-Day Restrictions

Regulation F also restricts the times at which debt collectors are allowed to text consumers. Allowed local times are 8:00 a.m. to 9:00 p.m. for the consumer. These apply across phone calls, text messages, and emails.

To comply with debt collector text message regulations, time zone determination in national portfolios needs automation to avoid compliance risk. Unknown consumers should be moved into conservative default time windows.

Prohibited Content in Text Messages

This sets out how can collection agencies text you. Anything intimidating, pressurizing, threatening, creating misleading urgency, disclosing details of the debt to third parties, and misuse of LCM (limited content messages) can be classed under prohibited content.

Under the disclosure clause, there is a unique challenge in the form of accidental disclosure. Modern smartphones display text messages as well as email alerts. These notifications can be accidentally viewed by unauthorized third parties, like co-workers or bystanders. Similarly, the ease with which messages can be screenshotted and shared is also a challenge, as they can be taken out of context and cause legal issues.

TCPA Compliance for Debt Collection Texts

Under the TCPA debt collector laws, explicit written consent is needed for autodialed messages, with opt-out options clearly mentioned, and these should be honored immediately. In addition, all messaging needs to occur between 8 a.m. and 9 p.m. in the recipient’s time zone. Violations can lead to heavy fines, making strict consent documentation necessary.

Express Consent vs. Prior Express Written Consent

In TCPA-compliant debt collection, Prior Express Consent is considered sufficient for automated informational calls like payment reminders, account updates made to cell phones.

This could be either verbal or written. When a consumer provides their phone number during account setup or initial communication, most forms authorize receipt of non-marketing, informational calls/texts.

Prior Express Written Consent (PEWC) is essential for marketing or promotional communications and requires a signed agreement. This explicitly authorizes calls/texts using an ATDS (automatic telephone dialing system) or pre-recorded voice for marketing. It must clearly state that consent is not a condition of purchase.

Autodialer Rules After Facebook v. Duguid

Under this ruling, Automatic Telephone Dialing System (ATDS) definition is narrowed further for the debt collector text message regulations. For a device to be an ATDS, it must have the capacity to use a random or sequential number generator to store or produce telephone numbers to be called.

Legacy systems are generally not considered ATDS because they do not randomly or sequentially generate numbers. The court ruling distinguishes between randomly dialing numbers and targeted, business-related, or informational calls.

Handling Consent Revocation

TCPA requires immediate honoring of consent revocation under “any reasonable means.” This includes usage of STOP keywords, email, and replies, as well as informal language. A simple collection text message example could be “stop texting me”.

Revocation should be implemented and systems updated ASAP, to prevent future automated text communications to that number. This can be challenging as assembling calling lists that differentiate between Do Not Call lists and the reassigned number database (RND) is an extensive process.

We discovered during an assessment that a client’s system was blocking debt collection calls using the national Do Not Call list, which does not apply to the debt collection industry.

Kompato AI offers a multi-layer defense architecture in the form of real-time API validation before each contact, reassigned number database scrubbing, and point-of-send suppression checks form the minimum standard for revocation enforcement to ensure that 99% of compliance violations are voided for most clients.

State-Level Text Message Regulations That Add Complexity

While the debt collector text message regulations exist, several states have more stringent requirements that include licensing prerequisites, stricter time windows, portfolio-specific prohibitions, and requirements for additional disclosures.

These tighter licensing, additional disclosures, stricter time windows, and channel regulations on SMS collections create an operational challenge for manual systems as all applicable state laws need to be factored in, as well as all debt collector text message regulations, before outreach to the consumer.

Manual enforcement for state-wise compliance can be a nightmare, especially when combined with licensing requirements. For example, in Massachusetts, one year of financials is needed before licensing, which delays market entry and creates coverage gaps for nationally-licensed organizations.

Where new portfolios are added on, accounts in unlicensed states must be swept before starting communications. This is where automated systems have an edge; they can configure their systems to exclude addresses from a specific state and adapt calling rules according to state-specific regulations. Kompato AI clients get state-wise compliance sweeps to ensure all communications meet regulations.

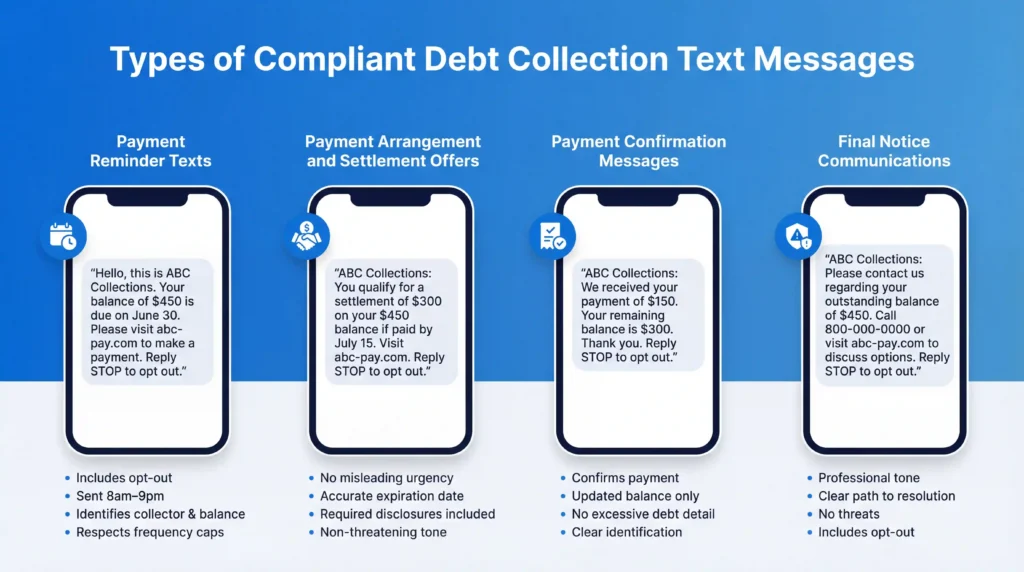

Types of Compliant Debt Collection Text Messages

Text messages that comply with debt collector text message regulations must include clear identification, the amount owed, and a simple “STOP” opt-out method. Types include:

Payment Reminder Texts

Reminder texts remind the consumer about the debt and request payment by the due date. The key requirements are:

- Include opt-out instructions.

- Follow the allowed hours timing of messages (8 am to 9 pm)

- Identify the collector and debt amount, and due date.

- Respect frequency caps.

- Ensure that the language used is friendly.

Payment Arrangement and Settlement Offers

Texts sent to offer different arrangements and settlement options should state the obvious debt and request the consumer to pay by any of the listed options. The key requirements under the debt collector text message regulations are:

- Avoiding misleading urgency and using non-threatening language

- Ensure settlement expiration dates are accurate.

- Include required disclosures.

Payment Confirmation Messages

These messages confirm receipt of the settlement amount and should avoid unnecessary debt detail disclosure to comply with debt collector text message regulations. These ideally just reflect the updated balance as well as the received amount.

Final Notice Communications

Since these can be highly liable to litigation, these notices need to be professional, clear, non-threatening, and include a direct path to resolution before escalating to legal action or agency transfer.

How Compliant Texting Improves the Debtor Experience

Compliant texting means following the FDCPA text messaging rules, and this can generally transform a traditionally intuitive process into a more transparent, and user-friendly experience. By linking SMS and other communications to regulatory frameworks like Regulation F and the TCPA, collectors can improve trust and engagement.

When consumers have opt-out as well as self-service options, and are communicated with under frequency limits, and at an appropriate time, they respond with more flexibility and are more likely to engage and pay.

Kompato AI applies the unified memory concept, and consumers get personalized and thorough messages that conform to compliance requirements and help its clients reduce FDCPA violations drastically.

How to build a Compliant SMS Collections Strategy

To comply with FDCPA text messaging rules, businesses need to follow the TCPA, the Fair Debt Collection Practices Act, and Regulation F. The key principles of these are based on ensuring consumers agree to being contacted, are contacted a limited number of times, and at reasonable times. SMS should have easy opt-out methods, and a detailed, tamper-proof audit trail of all communications should be available.

Capturing and Documenting Consent Properly

Proper documentation is the primary defense in both a TCPA lawsuit or regulatory audit. Businesses need to build in consent capture mechanisms in credit agreements, payment portals, calls, and post-call confirmations. Documentation tying the number to the consumer and the timestamp is essential for maintaining auditable trails.

Establish Audit Trails for Every Message

An audit trail is a verifiable proof of compliance. To be effective, the system must log every action automatically. Every text must be logged with a timestamp, content, recipient, consent record, opt-out and suppression status, frequency calculation, and time zone validation.

Beyond message logs, sophisticated programs maintain test coverage matrices, red-team scenario libraries, change control documentation, and compliance regression testing artifacts. A record of all communications ensures that they are easily searchable for reporting under FCRA law collections, TCPA class actions, and CFPB examinations.

Syncing Opt-Outs and Suppression Across Channels

A unified, automated system is needed to manage “STOP” requests. A CRM or specialized compliance module can act as the central repository for consent. When a consumer opts out via SMS, their status must instantly update in email, voice, and billing systems.

Once an opt-out is received, the system must immediately block further messages to that number to avoid TCPA lawsuits.

Reconfirming Consent on a Regular Cadence

To stay compliant while factoring in phone number reassignment, it is highly effective to renew consent every 60 days, although this is not a regulatory requirement. Automated systems can send a message and automatically pause messaging if the threshold passes without reconfirmation.

How AI Ensures Per-Message Compliance at Scale

AI-powered debt collection embeds regulatory rules directly into its workflows, which allows real-time monitoring to check, block, or adjust messages before they are sent. Collectors can handle thousands of accounts daily through automated debt collection systems while adhering to FDCPA, TCPA, and CFPB regulations.

These are things debt collectors cannot do, as human errors like miscounted frequency caps, violating time windows, or failing to check suppression lists are common.

In comparison, Kompato AI applies all compliance rules programmatically on every single SMS, email, and voice message simultaneously, delivering omnichannel compliance without operational overhead, raising the capability threshold significantly. Our three-layer compliance architecture solves the manual problems of frequency, channel selection, and timing.

We also offer real-time API validation with the client’s system before each contact attempt and point-of-send compliance checks against DNC, RND, and channel-specific suppression lists.

Kompato’s Approach to Compliant AI-Powered Text Collections

Kompato AI embeds compliance at the strategy layer, validation layer, and execution layer, ensuring every text meets federal and state requirements.

All FDCPA, TCPA, Regulation F, and other regulatory requirements are hard-coded in our system and enforced in real time across all interactions and touchpoints. Our compliance report shows 99.91% pass rate across 45 regulatory and internal policies. As a result, FDCPA violations have reduced to less than 1% for most of our clients.

Key capabilities include:

- Two-way AI-powered texting with real-time adaptive negotiation.

- Omnichannel compliance enforcement across SMS, email, and AI phone calls.

- Unified frequency caps and suppression lists.

- Channel optimization scoring — right channel, right time.

- Personalized payment portals with dynamic settlement delivery.

- Automated enforcement of FDCPA, TCPA, Regulation F, and specific state rules on every interaction.

- Instant scalability without incremental compliance risk.

- Support for first-party and third-party portfolios nationwide.

Connect with the Kompato AI team to explore how we deliver compliance and performance together in one intelligent platform.

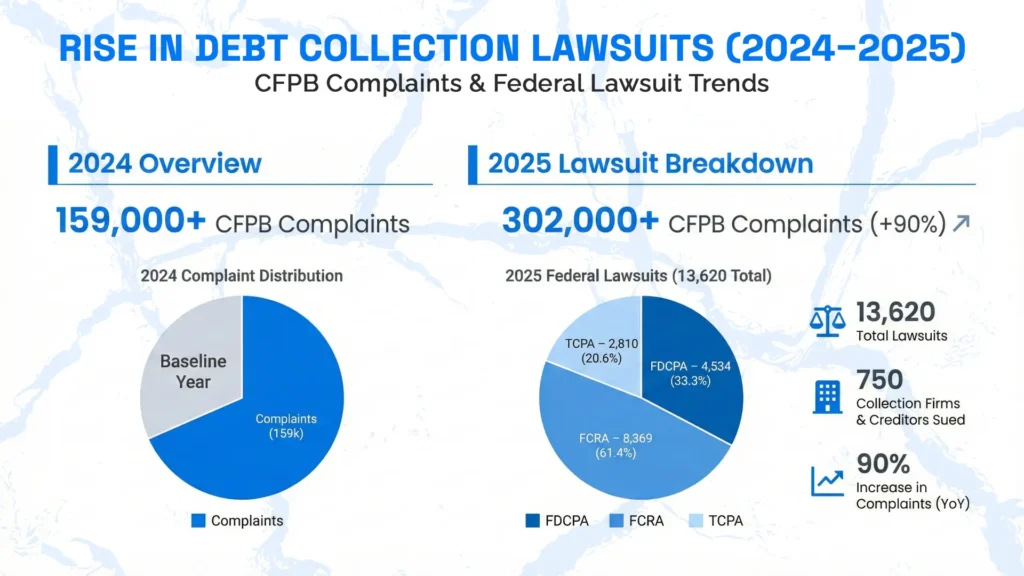

Consequences of Non-Compliance with Text Message Regulations

Non-compliance with debt collector laws can lead to severe consequences. The most severe of which are the fines of $500–$1,500 per every unauthorized text, as well as class-action lawsuits, and reputational damage.

Annual CFPB complaints against creditors and debt collectors increased 90% from over 159k in 2024 to over 302k in 2025. About 750 different collection firms and creditors were sued. A total of 13,620 lawsuits were filed in 2025 (4,534 FDCPA, 8,369 FCRA, and 2,810 TCPA).

With text messages, consumers have a permanent, easily discoverable record, and non-compliant texts are a litigation magnet. As the scale of debt collection expands with debt exposures, regulatory exposure is also scaling linearly.

Final Thoughts on Debt Collector Text Message Regulations

There is no question that text messaging is the channel with the highest ROI in modern collections so far, but only as long as it remains compliant with the debt collector text message regulations.

While these set down rules for how debt collectors are allowed to text you, messaging systems need to utilize compliance parameters for a competitive advantage. It needs to be incorporated into decision engines, suppression logic, and message governance, and be adaptable to adjust automatically as rules change.

Frequently Asked Questions

Yes. Regulation F explicitly permits electronic communications, including text messages, provided collectors comply with FDCPA, TCPA, and applicable state laws regarding consent, content, timing, frequency, and opt-out.

Under Regulation F, more than seven communications within seven consecutive days create a rebuttable presumption of harassment. Frequency must be calculated across channels, not in isolation.

As per the debt collector text message regulations, messages need to include collector identification, required disclosures (unless qualifying as limited-content), and a clear opt-out mechanism. Messages must avoid misleading or threatening content.

Consumers may opt out by replying STOP or using any reasonable method. Collectors must honor revocation promptly and suppress future messages.

The TCPA can impose statutory damages of $500–$1,500 per message, while Individual lawsuits under FDCPA can award up to $1,000 in statutory damages per lawsuit (not per violation), plus attorney’s fees and actual damages. CFPB enforcement can lead to civil money penalties and consumer restitution.

Yes. Licensing, time restrictions, disclosure requirements, and channel limitations vary. National portfolios must apply state-specific rules to each consumer.

AI platforms enforce frequency caps, time windows, consent validation, and suppression logic. They enable disclosure insertion programmatically, reducing human error and enabling scalable compliance.

TCPA governs consent and automated contact mechanisms, focusing on telephone dialing systems and statutory damages. Regulation F modernizes FDCPA for digital communication, addressing frequency, opt-outs, and disclosure structure. Both apply simultaneously.