The Fair Debt Collection Practices Act (FDCPA) governs nearly every structured interaction between third-party debt collectors and consumers in the United States. For collections leaders, the FDCPA functions as the primary blueprint for organizational design. It dictates the technical parameters of outreach programs, sets the hard limits for cross-channel communication, and serves as the core architecture for all compliance risk controls.

Originally enacted in 1977 and modernized through Regulation F in 2021, the FDCPA now explicitly addresses digital communication, including email and text messaging.

Understanding what is fair debt collection practices act and what is the purpose of the fair debt collection practices act is only the starting point. Violations of the act can trigger lawsuits, class actions, and regulatory enforcement, making it essential to operationalize compliance at scale.

What the Fair Debt Collection Practices Act (FDCPA) Actually Governs

The FDCPA governs how third-party debt collectors communicate with consumers and how collection activity must be structured. It regulates when collectors can make contact, how often they may reach out, what disclosures must be included, how validation notices are delivered, how disputes must be handled, and what conduct is prohibited.

The statute restricts false or misleading statements, harassment, unfair practices, and the disclosure of debt information to third parties. It applies to third-party collectors, debt buyers, and collection law firms collecting consumer debt, but generally not to original creditors or commercial obligations.

In 2024, the CFPB received more than 207,800 debt collection complaints, nearly double the prior year. Rising complaint volume increases litigation and enforcement exposure. In practice, the FDCPA shapes both behavior and systems, influencing contact controls, disclosure templates, dispute workflows, and suppression logic across collections operations.

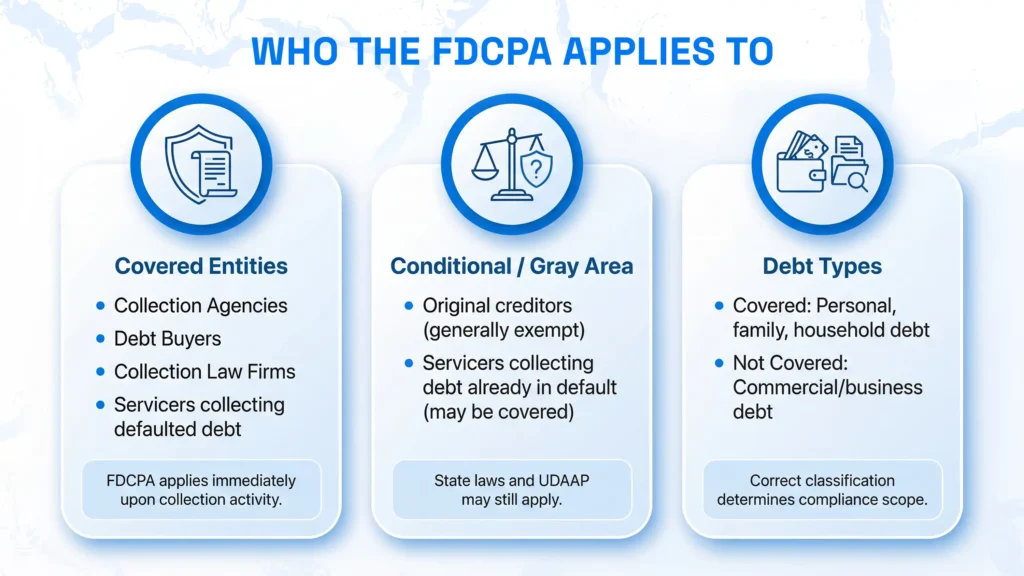

Who the FDCPA Applies To

Understanding who falls under the Fair Debt Collection Practices Act (FDCPA) determines which operational controls must be activated, which communication systems must be regulated, and where exposure begins. Leaders often ask what FDCPA stands for, but the more important question is: who qualifies for protection under FDCPA, and who qualifies as a covered collector?

Third-Party Debt Collectors

The FDCPA applies to anyone who regularly collects debts owed to another.

This includes collection agencies, debt buyers, collection law firms, and servicers collecting defaulted debt for another entity.

If an organization collects consumer debt on behalf of someone else, the FDCPA governs its communication limits, validation process, dispute handling, and FDCPA rules, including Mini Miranda FDCPA disclosure requirements.

Debt Buyers and Purchased Portfolios

When a company purchases charged-off receivables, it becomes a debt collector under the FDCPA. Obligations attach immediately.

But compliance for debt buyers starts before the first contact.

The critical gate is the pre-activation scrub. Before accounts move from “new” to “active”:

- Scrub for bankruptcy, deceased, and cease-and-desist flags

- Validate chain-of-title documentation

- Obtain fresh phone data (reassigned numbers create per-call exposure)

- Verify digital consent before initiating text or email

Inherited data decays quickly.

Contacting suppressed accounts creates scalable exposure under the FDCPA; the scrub gate prevents systemic violations before recovery begins.

First-Party Collections and the FDCPA Boundary

Original creditors collecting their own debts are generally not covered by the Fair Debt Collection Practices Act (FDCPA).

However, gray areas exist.

A servicer collecting debt already in default on behalf of another party may fall within scope. Additionally, state laws and UDAAP standards often mirror FDCPA rules, even where the statute does not technically apply.

For lenders with internal collections programs, understanding the framework of the FDCPA remains essential, even if the statute does not formally govern every interaction.

Types of Debt Covered

The FDCPA applies to consumer debts incurred for personal, family, or household purposes. It does not cover business obligations.

In other words, does FDCPA apply to commercial debt? Generally, no.

Accurate debt classification is critical. Mislabeling accounts can either create an unnecessary compliance burden or expose consumer accounts to risk under the act.

Core FDCPA Provisions Every Collections Operation Must Follow

The Fair Debt Collection Practices Act (FDCPA) does not just define prohibited behavior. It defines how outreach systems must be engineered. While many summaries of the FDCPA walk through statutory sections, operational leaders need to understand the law through execution risk.

Communication Restrictions and Contact Rules

Under the FDCPA, contact is generally limited to 8:00 a.m. to 9:00 p.m. Represented consumers must be contacted through counsel, workplace restrictions must be honored, and cease-communication requests require immediate compliance.

Most violations stem from system gaps rather than intent. FDCPA filings increased approximately 7-8% year-over-year in 2024-2025, reflecting breakdowns such as missed suppression flags or outdated data. Each improper contact may constitute a separate violation.

Effective compliance requires defined frequency and timing limits, real-time status validation, and point-of-send suppression controls.

Third-Party Disclosure Protections

The FDCPA prohibits revealing the existence of a debt to third parties. Collectors may seek location information, but cannot disclose that a debt exists.

Digital channels increase template risk. Subject lines, included addresses, and SMS preview text must not imply debt collection. A single email or screenshot can become evidence.

Harassment and Abuse Prohibitions

Section 1692d of the FDCPA prohibits harassment, including threats, obscene language, and repeated calls intended to annoy.

Operationally, this requires:

- Frequency controls configured below the 7-in-7 ceiling

- Cross-channel aggregation (phone, text, and email counted together)

- Script discipline and monitoring

In our experience, a growing risk is call baiting, where consumers or counsel provoke non-compliant responses. Manual QA detects issues after exposure occurs. Under the act, real-time escalation controls are essential to prevent violations driven by delay rather than intent.

False or Misleading Representations

Section 1692e of the FDCPA prohibits any false, deceptive, or misleading representation in connection with the collection of a debt.

The statute specifically identifies the following prohibited conduct:

- Falsely representing affiliation with the United States or any State.

- Falsely representing the character, amount, or legal status of a debt, or the compensation lawfully receivable.

- Falsely representing that any individual is an attorney or that a communication is from an attorney.

- Representing that nonpayment will result in arrest, imprisonment, seizure, garnishment, or sale unless such action is lawful and intended.

- Threatening action that cannot legally be taken or is not intended.

- Falsely implying that a transfer of the debt will cause the consumer to lose defenses or become subject to prohibited practices.

- Falsely implying the consumer committed a crime.

- Communicating credit information known to be false, including failing to note a disputed debt.

- Using communications that falsely appear authorized by a court or government agency.

- Using any deceptive means to collect or obtain information.

- Failing to provide required Mini Miranda disclosures (subject to the formal pleading exception).

- Falsely implying accounts have been turned over to innocent purchasers for value.

- Falsely representing that documents are legal process.

- Using a name other than the true name of the debt collector.

- Falsely representing that documents are not legal process or do not require action.

- Falsely representing that the collector operates or is employed by a consumer reporting agency.

Operationally, this requires strict scripting discipline, accurate balance validation, and controlled messaging. AI-generated communications must be deterministic and tied to verified account data. Even minor inaccuracies can create statutory exposure.

Unfair Practices

Section 1692f of the FDCPA restricts unfair practices such as collecting unauthorized amounts, prematurely depositing post-dated checks, or threatening action without legal basis.

In our experience, these are system-level risks. Payment workflows must prevent unauthorized fees, settlement logic must be enforceable, and post-dated instruments must be tracked automatically.

The FDCPA regulates not only what agents say, but also how balances, payments, and settlement systems operate. In modern collections, compliance must be engineered, or exposure follows.

Debt Validation and Consumer Dispute Rights

The Fair Debt Collection Practices Act (FDCPA) treats validation and dispute handling as core compliance obligations.

Operational failures typically stem from a mismatch between workflow velocity and statutory deadlines. Even when verification is granted, the inability to process data at the speed required by law creates significant compliance gaps.

Required Validation Notice Content

Under § 1692g of the FDCPA, collectors must send an initial validation notice containing:

- The amount of the debt

- The name of the current creditor

- A statement of the consumer’s right to dispute

- A 30-day dispute window

Regulation F enhanced these requirements. The modern notice must also include:

- An itemization date

- Clear breakdown of interest and fees

- Truncated account number formatting

- Option to use the CFPB model validation notice

These enhancements standardize disclosure but also increase template risk. Modern validation letters function as structured compliance instruments. Under the act, these documents have evolved into data-driven tools that must align with specific regulatory architecture to remain defensible.

Handling Disputes and Verification Requests

When a consumer disputes a debt, the FDCPA requires the collection to stop until verification is provided.

Operational risk arises when dispute intake and suppression are not synchronized. Manual workflows often delay system-wide updates while documentation is routed to original creditors. Any contact during that gap may violate the act.

For purchased portfolios, verification may require a chain-of-title review, further extending timelines.

Dispute intake must be channel-agnostic. Whether received by phone, letter, email, or portal, it should trigger immediate suppression across all channels. AI-native systems like Kompato AI enforce this automatically, eliminating latency between dispute receipt and suppression.

Mini-Miranda Disclosure Requirements

The FDCPA Mini Miranda requires collectors to disclose that “this is an attempt to collect a debt” in communications with consumers.

Implementation varies by channel:

- Phone calls: Scripted disclosure at the start

- Emails: Typically placed near the top with the collector identity

- Text messages: Must fit within character limits

- Letters: Standardized inclusion

- Portals: Depends on access path and legal interpretation

Whether interaction through a portal constitutes a “communication” under the FDCPA remains unsettled and should be reviewed with counsel. State-specific disclosure requirements add additional complexity.

At scale, a missing disclosure in even one template can multiply into thousands of violations. Effective compliance embeds disclosure logic across all entry points rather than relying on manual insertion.

How Regulation F Modernized the FDCPA

The CFPB’s 2021 Regulation F is the most significant modernization of the Fair Debt Collection Practices Act (FDCPA) in decades.

It did not replace the statute, but clarified how it applies to modern collections, particularly as digital evidence, replayability, and explainability become core enforcement expectations as the future of AI in debt collection shifts toward auditable and replayable systems.

Digital Communication Under Regulation F

Regulation F explicitly brought texts, emails, and certain social media activity into the FDCPA compliance framework. It also formalized requirements that create direct operational implications:

- Clear opt-out pathways for electronic communications

- A “limited-content message” concept for voicemail-style communications designed to avoid third-party disclosure

- Frequency presumptions that must be managed across channels

In practice, Reg F turns digital outreach into template engineering. Subject lines, preview text, opt-out logic, and disclosure placement become compliance controls under the statute.

The 7-in-7 Contact Rule

Regulation F presumes that more than seven communications within seven days about a debt, or contact within seven days of a conversation, may constitute harassment.

The 7-in-7 Contact Rule applies specifically to telephone calls. The rule applies per debt, not per consumer, meaning multiple debts can increase exposure. While the rule is limited to phone calls, operational risk increases when outreach systems fail to coordinate across channels, which may eventually create cumulative consumer fatigue and potential UDAAP exposure.

Most operations treat 7-in-7 as a ceiling. Violations typically arise when outreach systems and records fall out of sync.

Updated Validation Notice Requirements

Regulation F also expanded validation notice requirements under the FDCPA. It clarified the itemization date requirement, increased required information fields, and introduced a model validation notice format.

For operations, this means validation notices are no longer simple letters.

They are structured outputs that require:

- Accurate data mapping (balances, fees, interest)

- Account number truncation logic

- Document version control and proof of delivery

- Repeatable generation workflows that do not drift across portfolios and clients

Reg F raised the bar on what “good enough” looks like, and it pushed FDCPA compliance deeper into systems, templates, and orchestration.

FDCPA Compliance Across Digital Channels

Modern collections occur across phone, SMS, email, portals, and sometimes social media, and AI in debt collection increasingly sits inside that omnichannel execution layer where orchestration and compliance architecture must work together.

The Fair Debt Collection Practices Act (FDCPA) applies across each channel, but the risk profile differs by medium.

Compliance is now journey-specific.

Text Message and SMS Compliance

SMS creates heightened third-party disclosure risk. Message previews can appear on locked screens, meaning any content revealing a debt may violate the FDCPA.

Operational constraints include:

- Including Mini Miranda FDCPA disclosures within 160-character limits

- Clear opt-out mechanisms in every thread

- Verifying TCPA consent before first digital outreach

- Ensuring unsubscribe flags suppress future attempts instantly

Character limits represent a fixed legal boundary that governs every outreach attempt and ensures statutory adherence.

Email Collection Compliance

Email collection must comply with disclosure and opt-out requirements under the FDCPA and Regulation F.

The primary risks arise from employer-monitored inboxes, shared household devices, subject lines that imply debt collection, and the inclusion of debtor mailing addresses, which can increase third-party disclosure exposure.

As a protective practice, many operations omit debtor addresses in email templates while still retaining required disclosures such as the FDCPA Mini Miranda. Every email should be written with the assumption that it may be forwarded, screenshotted, or produced in litigation.

Phone and Voicemail Rules

Phone outreach remains heavily regulated under the FDCPA.

Key controls include:

- Cross-channel frequency tracking under Regulation F

- Use of limited-content messages for voicemail

- Script adherence for all calls

- Monitoring and recording policies

AI-powered calling systems must comply with the same scripting guardrails as human agents. Deterministic disclosures and real-time guardrails are essential to ensure the statute is followed on every interaction.

How to Build FDCPA-Compliant Collections Operations

The Fair Debt Collection Practices Act (FDCPA) cannot be implemented through policy alone. It must be embedded in systems architecture.

Compliance Controls and Monitoring Systems

Effective compliance requires a layered defense, especially in automated debt collection, where enforcement logic, orchestration, and logging must function as a single system under volume rather than as isolated controls.

- Strategy controls: Configure frequency limits, channel restrictions, and time-of-day windows per client and portfolio.

- Pre-execution validation: Perform real-time checks before contact to catch disputes, bankruptcies, cease-communication requests, or representation updates.

- Point-of-send suppression: Apply DNC checks, reassigned-number validation, and opt-out enforcement at execution.

In our experience, violations of the FDCPA occur in the gaps between these layers.

Configuration must be client-specific. Different risk postures require configurable logic without drift.

Monitoring alone is insufficient.

Tools that flag issues without defined remediation SLAs create discoverable evidence of known problems. Effective systems pair automated alerts with designated owners and time-bound resolution requirements.

We consistently notice that proactive FDCPA assistance, whether legal, operational, or technology-driven, reduces systemic risk far more effectively than reactive remediation.

Documentation and Audit Readiness

Under the FDCPA, audit readiness is evidence-based. A defensible compliance program should include documented test coverage across validation, disputes, bankruptcy, credit reporting, and third-party disclosure, along with clear escalation procedures and change-control policies.

Every interaction must be logged with full metadata, and recordings should be exportable with defined retention standards.

Regulatory scrutiny centers on the actual legality of each interaction. A library of policies offers no defense if the execution fails to meet FDCPA standards in the field.

Kompato AI maintains structured, exportable audit trails by default, supporting examination readiness and defensible record-keeping.

Training, Quality Assurance, and Consistent Execution

Manual QA sampling alone cannot reliably guarantee compliance at scale. Even scoring tools that evaluate every call create a remediation bottleneck if leadership escalation is delayed.

Consistency requires programmatic enforcement:

- Real-time guardrail checking on every utterance

- Automated suppression upon dispute intake

- Uniform disclosure logic across channels

There is an operational tradeoff between response speed and compliance certainty. Real-time checking introduces slight latency. But unverified responses create exposure under the FDCPA.

Organizations relying solely on manual review almost certainly have undiscovered compliance risk in their historical interaction data.

How Can You Leverage AI to Maintain FDCPA Compliance at Scale

The Fair Debt Collection Practices Act (FDCPA) requires consistent enforcement across every interaction and channel.

Manual processes do not scale, and the structural differences between AI debt collection and traditional methods become most visible when automation accelerates variability instead of constraining it through deterministic enforcement.

AI platforms like Kompato AI enforce FDCPA requirements programmatically, embedding disclosures, frequency controls, suppression logic, and audit trails directly into the interaction engine.

Core controls include automated Mini Miranda insertion, real-time cross-channel frequency tracking, time-zone-aware contact limits, guardrailed scripting, and instant suppression upon dispute.

In controlled deployments, Kompato AI has demonstrated 13% higher liquidation rates by months 4-6 compared to human agents, with under 1% escalation and zero compliance exceptions within defined parameters.

Strategy controls, real-time validation, and point-of-send suppression embed compliance directly into the system architecture. This framework eliminates the need for manual oversight on every interaction.

Under the FDCPA, the question is no longer compliance or performance, but how to achieve both simultaneously. When enforcement is deterministic, operators can apply successful debt collection techniques to maximize recovery rates without increasing exposure under the act.

Kompato’s Approach to FDCPA-Compliant AI Collections

The operational problems surfaced throughout this guide—such as multi-channel complexity, system lag, disclosure drift, and cross-channel frequency aggregation—are precisely the problems Kompato AI was built to solve.

Kompato AI enforces the Fair Debt Collection Practices Act (FDCPA) across every interaction, automatically.

Key differentiators include:

- True conversational AI: Handles real dialogue, not rigid scripts. It adapts to borrower context in real time, improving outcomes in complex or sensitive interactions.

- Compliance built into architecture: FDCPA, Regulation F, TCPA, and state rules are hard-coded and enforced in real time across all interactions. Deterministic guardrails and automated suppression drive a 99.91% pass rate across 45 regulatory and internal controls.

- Unified omnichannel memory: Voice, SMS, and email operate on shared context, eliminating fragmented borrower experiences and improving continuity.

- Rapid performance ramp: Demonstrated 70% human-level performance within seven weeks, accelerating ROI and reducing pilot risk.

- Scalable engineering backbone: Backed by a 150+ engineer infrastructure team, enabling fast scale from pilot to enterprise volume without compliance drift.

Compliance is a core architectural component, engineered directly into the system’s foundation.

See how Kompato ensures FDCPA compliance on every interaction across every channel – book a demo.

Consequences of FDCPA Violations

Violating the Fair Debt Collection Practices Act carries measurable risk. Consumers may recover actual damages plus up to $1,000 in statutory damages per case, along with attorney’s fees. Class actions may result in statutory damages up to $500,000 or 1% of net worth, whichever is less. The CFPB may impose civil money penalties and operational restrictions, while state attorneys general and the FTC may pursue parallel enforcement.

According to the Federal Trade Commission (FTC), the agency has sued more than 30 debt collection companies for unlawful practices, banning some from the industry and imposing substantial penalties. In 2021 alone, FTC enforcement actions resulted in over $4.86 million in refunds to consumers.

Digital collections increase exposure. Texts, emails, and portal screenshots create permanent, discoverable evidence, meaning a single template error, such as a missing Mini Miranda, incorrect balance, or improper subject line, can scale into class action liability.

As collections scale, so does regulatory risk. Compliance is now a core operational discipline.

Final Thoughts on the Fair Debt Collection Practices Act

The FDCPA is not merely consumer protection legislation, but the operational blueprint for compliant collections in the United States. It defines how organizations communicate, validate, document, and resolve accounts. Regulation F extended that framework into digital channels with the same rigor long applied to phone and mail.

Understanding what FDCPA stands for is far less important than operationalizing it at scale. The organizations that succeed treat it as systems architecture, embedding controls into technology rather than relying solely on manual oversight. As omnichannel collections expand and regulatory scrutiny intensifies, the compliance bar will continue to rise, and the cost of falling short under the FDCPA will only grow.

Frequently Asked Questions

A federal law regulating how third-party collectors pursue consumer debt, including rules for communication, validation, and dispute handling. Regulation F expanded coverage to digital channels such as email and text.

Third-party collectors, debt buyers, and collection attorneys collecting consumer debt. Original creditors are generally exempt.

Excessive contact, failure to validate, false or misleading statements, improper third-party disclosure, and contacting consumers at prohibited times.

Yes. Regulation F requires disclosures, opt-outs, and frequency controls for digital communications.

More than seven communications (including telephone calls and voicemail attempts) within seven days about a debt, or contacting a consumer within seven days after a live conversation, may be presumed harassment.

Yes. Debt buyers are classified as debt collectors and must comply from the moment they acquire a portfolio.

Consumers may recover actual damages plus up to $1,000 per case. Class actions may reach $500,000 or 1% of net worth, plus attorney’s fees and regulatory penalties.

AI enforces disclosures, frequency limits, suppression logic, and audit trails automatically across channels.