The omnichannel vs multichannel communication debate in debt collection explores how omnichannel can be a performance and compliance game-changer. Traditional multichannel approaches apply phone calls, emails, SMS, and portal messages across isolated systems, often creating fragmented borrower experiences and limited visibility.

In comparison, omnichannel strategies unify all channels into a single, data-driven ecosystem so that every interaction is informed by past engagement and real-time insights. This results in improved contact rates, reduced friction, and ultimately drives stronger, more predictable recovery outcomes.

For creditors and collection leaders, this difference is about a smarter, coordinated communication process that increases recoveries up to 25%, reduces friction, and strengthens compliance.

This article explores the operational, technological, and compliance differences between multichannel and omnichannel communication. We’ll also cover how to evaluate, implement, and optimize the omnichannel model for modern recovery operations.

What Multichannel Communication Means in Collections

Multichannel means using more than one communication channel, but with no assurance that those channels coordinate. Agencies deploy multiple channels to increase reach and improve contact rates as and when needed. Most operations function within what can be described as a “blind channel” pattern, where communication streams cannot see or incorporate each other’s activity.

A typical multichannel stack includes a dialer platform (e.g., TCN), a standalone SMS vendor, an email service, and a separate letter vendor. Each runs distinct campaigns, maintains separate data environments, and operates under its own compliance controls.

The result is fragmentation with overlapping outreach, inconsistent messaging, duplicated effort, elevated compliance exposure, and higher operational overhead.

How Multichannel Collections Typically Operate

In practice, multichannel collections are operationally heavy. Each morning, teams load separate dialer campaigns, generate SMS worklists, schedule independent email blasts, and queue letters through a different fulfillment system.

While this appears diversified on the surface, it creates recurring manual overhead that compounds daily.

- Dialer campaigns are rarely “set and forget.” Operations teams continuously recalibrate worklists to determine which accounts feed live, adjusting suppression rules and contact priorities manually.

- SMS lists frequently require manual compilation because opt-out data does not sync seamlessly across vendors.

- Email platforms often rely on batch ETL processes instead of real-time APIs. These batch processes can delay consent updates and increase compliance exposure. Active sender rotation, domain warming, and IP reputation management are functions that many collections teams underinvest in.

What is critical is that these fragmented multichannels introduce data-quality traps. Call disposition codes may conflict across dialer, telephony, and CRM systems, where one call may be logged as both “busy” and “answering machine.” SMS-to-portal tracking is often unreliable, with automated scans or proxy clicks inflating engagement metrics.

Kompato AI applies safeguards to enforce contact frequency caps, state-by-state licensing filters, and automated disclosures, backed by timestamped logs across every channel.

Where Multichannel Falls Short in Recovery

Multichannel communication is still better than traditional, single-channel debt collection. However, since it operates channels independently, it creates a disjointed, impersonal, and sometimes overwhelming experience that fails to maximize and can even hurt recovery rates.

A debtor may call after getting an email, yet the agent has no visibility into any prior digital engagement. A multichannel collections strategy rarely adapts dynamically to response behavior that results in repeated outreach through underperforming mediums.

Compounding this issue is the declining effectiveness of individual channels. Email deliverability in collections faces aggressive spam filtering. SMS from unfamiliar numbers is increasingly ignored. Unknown outbound calls are frequently rejected. Each channel has a declining ceiling when used in isolation. No single touchpoint can drive engagement on its own.

Multichannel debt recovery operations also experience the “human taper” effect. Early-stage inventory receives heavy effort, while the long tail of recoverable accounts is progressively underworked, creating a predictable recovery plateau.

The measurable consequence is lower lifetime liquidation. Sustainable performance increasingly depends on omnichannel collections strategy orchestration with a unified consumer memory, coordinating voice, SMS, email, and letters. A successful debt collection channel strategy is about ensuring they work together intelligently and consistently.

What Omnichannel Communication Means in Collections

Omnichannel communication in debt collection integrates all communication channels into a single, unified, and data-driven platform to provide a seamless and consistent consumer experience. Unlike multichannel approaches, it allows for context-driven, consistent interactions across channels that improve engagement, payment success, and regulatory compliance.

In an omnichannel vs multichannel communication comparison, omnichannel goes beyond simply integrating channels. When implemented correctly, it creates a unified debtor journey supported by shared context, adaptive routing, and a consistent compliance posture across every touchpoint. In practical terms, omnichannel automated debt collection means every interaction across channels is connected to the same system of record.

The technical foundation of omnichannel communication collections is a “unified memory” of the consumer. This is a causally ordered event pipeline that records every interaction across every channel into a single account history. Each channel reads from and writes to this shared record. As a result, an AI call agent can see which emails were opened, which SMS links were clicked, what portal pages were viewed, and whether a hardship option was previously offered, before the conversation even begins.

The Unified Debtor Journey

The difference between omnichannel and multichannel communication in debt collection is a transformative, digital-first approach to recovering overdue payments. By moving away from siloed, calendar-driven outreach models, organizations are adopting an integrated strategy, which is called the Unified Debtor Journey. This leverages communications across channels and self-service portals to deliver a seamless, 24/7, and less intrusive experience.

In a true omnichannel collections strategy, the journey is event-based, not calendar-based. Triggers are behavioral signals like “SMS link viewed,” or “portal session started,” rather than static timelines that multichannel debt recovery yields like “Day 3.”

Take a multichannel vs omnichannel example:

- In a multichannel communication model, a debtor clicks a payment link in an email but doesn’t complete the transaction. The signal is captured in the email platform, but it doesn’t influence the broader strategy. Outreach continues as originally scheduled, a generic call or another templated message, with no adjustment based on the partial engagement.

- In omnichannel models, this abandoned payment attempt becomes a trigger. The system recognizes high intent and will send a personalized SMS referencing the same balance with a simplified payment link. If the debtor replies asking about installment options, the conversation is logged within a unified account record. Should the account later move to a live call, the agent sees the full interaction history: email engagement, SMS exchange, and prior payment attempts, so that the conversation picks up where the last touchpoint ended. Each interaction informs the next, creating continuity, context, and a higher probability of resolution.

The advantage of using omnichannel strategies comes from the consumer intelligence that links these signals into a real-time orchestration layer that adapts outreach dynamically. This strategy improves the consumer experience and boosts payment arrangements by up to 25% when digital engagement and follow-ups are aligned.

What True Omnichannel Requires Beyond Technology

True omnichannel debt collection is not an expansion strategy, but an operating model. It requires a unified data layer giving every touchpoint access to the same continuously updated account history.

At its core is a centralized decision interface that determines which accounts are contacted, via which channel, and in what order. Accounts carry eligibility flags, dynamic prioritization scores, and channel selection is assigned logically.

Compliance is centralized. Each channel has its distinct rules, TCPA for calls and SMS, CAN-SPAM for email, and Regulation F for contact frequency. A unified compliance engine enforces account-level limits, manages consent, and applies global suppression logic. Centralized orchestration and compliance turn omnichannel from a risk into a tool for precise, controlled recovery.

Omnichannel vs Multichannel Communication -Five Critical Differences

The difference between omnichannel and multichannel is a question of performance architecture. Multichannel debt collection runs channels in parallel but independently, leading to duplicate touches, calendar-based campaigns, inconsistent compliance controls, and the “human taper” where long-tail accounts lose pressure.

Omnichannel offers coordinated, behavior-triggered sequencing, informed by prior engagement. The result is smarter scaling without proportional headcount growth, lower cost per dollar collected, and more predictable recovery performance.

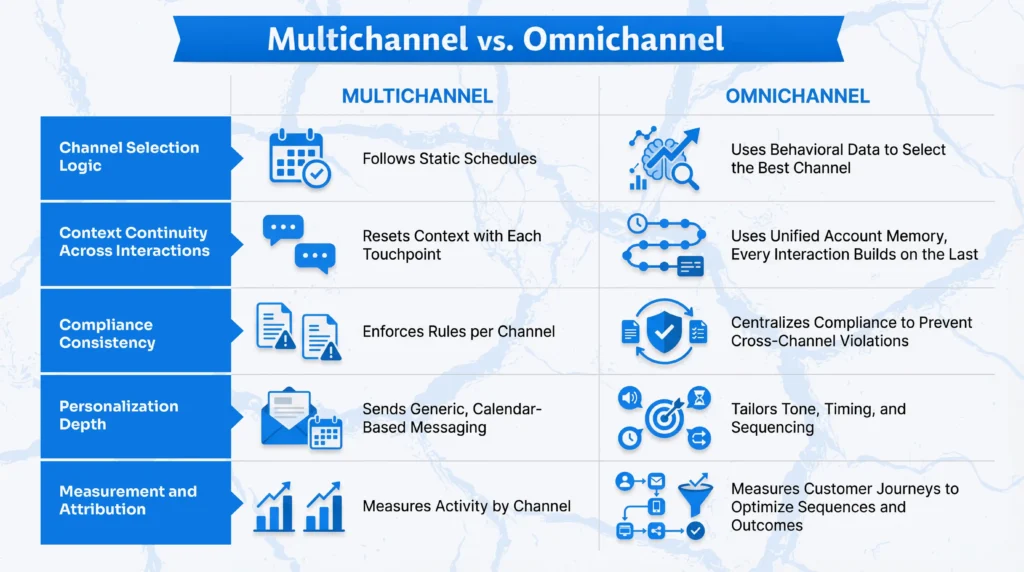

Channel Selection Logic

Multichannel debt recovery relies on static rules (e.g. call on day 3, text on day 7) without regard for engagement signals or account-specific behavior. Channels operate in isolation, duplicating effort, wasting resources, and creating inconsistent experiences.

Omnichannel debt collection uses dynamic, data-driven channel selection. Every account interaction, such as email opens, SMS clicks, and portal visits, is captured in a unified memory. The system identifies patterns from this memory, which channel a borrower responds to, when they are most active, how quickly they engage after outreach, and whether they convert after certain touchpoints.

If historical data shows higher responsiveness to SMS in the evening, outreach shifts there. If emails are opened but not clicked, messaging and sequencing adjust before escalating.

AI omnichannel collection applies conservative escalation; lower-cost, high-engagement channels are prioritized first, and escalation to voice calls or letters occurs only when engagement signals weaken or risk indicators increase.

Companies with extremely strong omnichannel customer engagement retain, on average, 89% of their customers, compared to 33% for companies with weak omnichannel customer engagement.

Context Continuity Across Interactions

Context continuity in the debt collection channel strategy ensures every channel is informed by the account’s interaction history. Omnichannel strategies log emails, SMS, portal visits, and payment attempts in a unified record so that human agents or AI can engage with full context visibility.

This avoids repetitive questioning, preserves debtor trust, and creates seamless, personalized recovery. In an omnichannel vs multichannel communication comparison, the differentiating advantage is sustained context. Omnichannel models maintain a continuous account history across every touchpoint, while multichannel approaches often reset the conversation with each channel.

Compliance Consistency

In most multichannel operations, compliance is often siloed, phone follows TCPA, email follows CAN-SPAM, SMS follows separate rules, leading to contacts that comply individually but violate overall frequency limits.

Under the widely accepted industry interpretation of Regulation F’s “7-in-7” rule, voice mail and phone calls together count toward the weekly cap, but multichannel systems track limits per channel. Similarly, TCPA consent differs by channel: phone consent does not automatically extend to SMS, and state-level variations require explicit opt-ins.

In the omnichannel vs multichannel communication discussion, the key difference lies in coordination, intelligence, and compliance management across channels. Traditional multichannel approaches operate each channel in isolation. AI-driven omnichannel collections centralize compliance at the account level, enforcing frequency caps, consent status, quiet hours, and channel-specific rules across all touchpoints.

Kompato AI, for instance, automatically scores every interaction against 45 compliance checkpoints (FDCPA, TCPA, Reg F) and deterministically provides consistent coverage across 100% of interactions. This improves contact strategy, reduces friction, and ultimately drives stronger, more predictable recovery outcomes.

Personalization Depth

In traditional vs. modern debt collection channels, the difference lies in personalization. Traditional outreach strategies send the same message to all debtors on each channel, with minimal adaptation, which lowers engagement. However, modern omnichannel approaches use behavioral data, payment history, and engagement signals. Outreach adapts dynamically, adjusting timing, tone, and escalation based on the debtor’s likelihood to respond, resulting in higher engagement, faster resolution, and stronger compliance through account-level orchestration.

Today, with multiple communication touchpoints (SMS, voice call, email, portal, live chat), 90% of consumers expect personalization and uniformity in communication across all channels.

In omnichannel vs multichannel communication, the key difference lies in how account-level intelligence drives outreach. Multichannel treats each channel in isolation and applies generic schedules and messaging without regard for past behavior or engagement. Omnichannel strategies use profile data, past interactions, and even emotional cues to tailor tone, timing, and channel sequence for each debtor. This personalized approach helps re-engage hard-to-reach accounts, improves contact rates, increases payment plan uptake, and offers more effective negotiations.

Measurement and Attribution

In multichannel operations, measurement is limited to channel-level metrics without assessing the interactions driving payment. Most systems default to “last channel outreach before payment” attribution, giving credit to the final touchpoint regardless of its true causal impact. This creates an attribution crisis, misallocating credit and obscuring truly effective channels or sequences.

In omnichannel vs multichannel communication, the difference lies in how interactions are tracked and analyzed. Multichannel approaches typically measure activity at the channel level. Meanwhile, omnichannel strategies track every interaction across all channels by capturing journey-level metrics. With full visibility across interactions, teams can see which channel sequences actually lead to resolution. Hence, they can refine strategies and tailor outreach to different debtor segments based on what truly works.

Businesses using AI omnichannel communication in collections are reporting up to 40% reduction in operating costs. By measuring performance in one unified system, collections leaders gain clearer forecasts, stronger operational efficiency, and better visibility into ROI. This clarity helps them direct resources toward the touchpoints that truly move accounts toward resolution.

How to Move From Multichannel to Omnichannel — A Practical Roadmap

Transitioning from multichannel to omnichannel means moving from presence on multiple, siloed platforms to delivering a cohesive, integrated, and customer-centric experience over all channels. The benefits are clear: improved engagement, up to 28% higher recovery rates, and reduced compliance risk.

Tools like Kompato AI streamline this process by unifying interactions, automating channel selection, and providing actionable insights across every touchpoint, making the shift faster, smarter, and more efficient.

Assess Your Current Channel Maturity

Before implementing an omnichannel collections strategy, it’s critical to audit your existing communications ecosystem. This is a core checklist to follow:

1. Interaction Visibility:

Can you see, in one central view, every contact made to a debtor across all channels in the last 7 days? In a debtor call, can the agent see the last email, SMS, or portal interaction, including opens, clicks, or abandoned sessions?

2. Compliance Enforcement:

Are Regulation F contact frequency limits enforced across required channels at the account level, or just per channel? Are channel-specific consent rules (TCPA for calls, CAN-SPAM for email, SMS opt-in) managed centrally or siloed?

3. Data Flow Audit:

Map every system handling debtor communication. For each pair: does data flow? Is it real-time or batch? What is the lag?

Identify “blind channels” where context is lost, creating gaps in attribution and strategy.

4. Channel Eligibility Audit:

For each account, can you determine which channels it’s eligible for today?

Or is eligibility managed in separate systems, preventing coordinated outreach?

Completing this checklist delivers actionable insights into operational and compliance gaps and enables data-driven decisions for daily and real-time orchestration.

Unify Your Data Before Your Channels

After assessing your channel’s maturity, the next step is to connect your data to create a centralized system. Attempting interconnections across channels without a unified view risks misaligned messaging, lost context, and compliance gaps.

Unified data requires a minimum of a causally ordered, account-level event table (aka “account histories”) that logs every interaction across all channels. This table should include:

- Account ID: unique identifier for each debtor

- Event timestamp: precise timing of the action

- Channel: email, SMS, call, portal, letter, etc.

- Event type: email sent, SMS clicked, call disposition

- Outcome: success, failure, partial engagement

- Eligibility flags: which channels the account can receive messages through today

This shared data foundation gives every channel access to the same source of truth, so outreach stays coordinated, compliant, and context-aware. A single account record supports both batch and real-time outreach, strengthens oversight, and improves measurable recovery results.

Start With AI-Powered Orchestration, Not Manual Integration

A common pitfall while implementing omnichannel communication is the “duct tape” approach, manually linking dialers, SMS, email, and portals with scripts and spreadsheets. In contrast to true omnichannel strategies that unify channels and automate account-level orchestration, this manual method creates fragile, person-dependent systems. In such dependent systems, minor errors or staff changes can break workflows, leading to missed contacts, lost context, and increased compliance risks.

Manual integration often manifests as Python scripts moving files between systems daily, worklists rebuilt and recalibrated manually every day, or using spreadsheets to track account eligibility across channels.

In contrast, modern AI collections solutions like Kompato AI provide true omnichannel capabilities from day one, automatically routing accounts across all channels based on behavior, risk, and engagement signals. By starting with AI, organizations avoid brittle manual dependencies, reduce errors by 20%, accelerate migration, and immediately gain scalable, compliant, and data-driven recovery operations.

Measure, Learn, and Optimize

The last and most important step is the continuous feedback loop, which is necessary for smarter, higher-yield recovery. Tracking outputs like “emails sent” isn’t enough; true optimization measures both first-touch impact and cumulative results across channels.

Some key measurement principles for omnichannel optimization are:

- Attribution Beyond Last-Touch: Start with first-engagement attribution and track each channel’s marginal contribution throughout the debtor journey.

- Shapley Value Analysis: Quantify each channel’s unique impact by comparing outcomes when it’s present versus absent in different touchpoint combinations.

- Holdout Experiments: When volume permits, create test cohorts, some exposed to all channels, others with one channel removed to identify real performance drivers.

- Signal Quality: Track meaningful engagement, not vanity metrics. For example, measure “email opened AND subsequent action within 48 hours” rather than clicks alone to avoid inflated counts from automated activity.

This framework helps collection teams refine the order, timing, and personalization of outreach, using insights from each interaction to improve recoveries while maintaining full compliance.

Why Leading Collections Operations Choose Kompato

Kompato AI embodies the practical success of omnichannel communication through coordinated, account-level intelligence and dynamic channel selection that outperform the traditional siloed approaches of multichannel routes. Its omnichannel process solves specific operational and compliance challenges that multichannel collections leaders face, including:

- Unified Debtor Memory: Every interaction, whether emails, SMS, calls, portal visits, or letters, is captured in a causally ordered account-level event pipeline for context continuity and to prevent lost negotiation history.

- Cross-Channel Compliance Engine: A centralized compliance layer enforces Reg F, TCPA, CAN-SPAM, and per-channel consent rules across all touchpoints, reducing legal risk and maintaining audit-ready records.

- AI-Powered Orchestration: The decision engine assigns accounts to channels dynamically based on debtor behavior, risk segment, and responsiveness history, following the conservative escalation principle. It supports both daily batch planning and real-time event-driven triggers for optimal engagement without manual recalibration.

- Human-AI Fusion: High-value, high-propensity accounts receive human attention where it matters most, while AI consistently manages the long tail of smaller or harder-to-reach accounts, maintaining pressure day after day without fatigue or deprioritization.

- Journey-Level Attribution and Analytics: Integrated measurement captures the marginal contribution of each channel, enabling data-driven optimization of sequencing, messaging, and overall recovery strategy.

Kompato AI shows how omnichannel debt collection can scale efficiently with selective human intervention, preserving compliance, maintaining context, and delivering measurable recovery outcomes.

The Future of Channel Strategy in Collections

The future of debt collections is clear: the voice-first with digital bolt-ons approach is giving way to digital-first strategies with intelligent voice deployment, where calls add unique value. In the omnichannel vs multichannel communication context, the future lies in moving beyond interlinked channels to hyper-personalization powered by real-time monitoring and predictive analytics.

Instead of static sequences, accounts will be continuously evaluated against engagement signals, payment behavior, risk factors, and even emotional cues to deliver the right message, on the right channel, at the right time.

Early investment in event pipelines and unified data builds a strong foundation by producing high-quality insights that improve performance and create efficiencies competitors may struggle to match. As AI capabilities, stronger data practices, regulatory alignment, and digital-first expectations converge, AI debt collections are evolving into a more strategic, analytics-driven, and scalable function.

Conclusion

The operational difference between omnichannel and multichannel isn’t the number of channels, but whether they share context, coordinate timing, and enforce compliance as a unified system.

The human taper effect shows multichannel underserves later-stage or lower-probability accounts, leaving recoverable dollars behind. Omnichannel maintains consistent engagement across the portfolio, reduces compliance risk, and improves attribution accuracy.

If you can’t see every contact across all channels in a single view, you’re still operating multichannel. Omnichannel is an operational architecture decision that determines whether recovery outcomes are predictable, scalable, and compliant.

To leverage omnichannel intelligence for smarter engagement, higher recoveries, and lower compliance risk, book a meeting right now with Kompato!