The third-party debt collection process plays a critical role in preserving liquidity, managing risk, and protecting balance sheets across lenders, FinTechs, B2C, and B2B businesses. Recently, the receivables portfolios have been growing in size and complexity, as unpaid debt increasingly distorts cash flow forecasts, prompting many organizations to rely on structured third-party collections.

The global debt collection services market is projected to grow steadily at a 3.2% CAGR through 2030, driven by rising delinquencies and increased outsourcing of recovery activities.

Today, traditional collection approaches are under strain, challenged by declining contact rates, rising compliance risk, and limited performance visibility. Modern debt collection models, built on data, analytics, and system design, improve recovery outcomes while reducing cost and risk. Understanding the third-party debt collection process is key to optimizing recovery, and platforms like Kompato AI are reshaping how collections are executed, making them more efficient, compliant, and scalable.

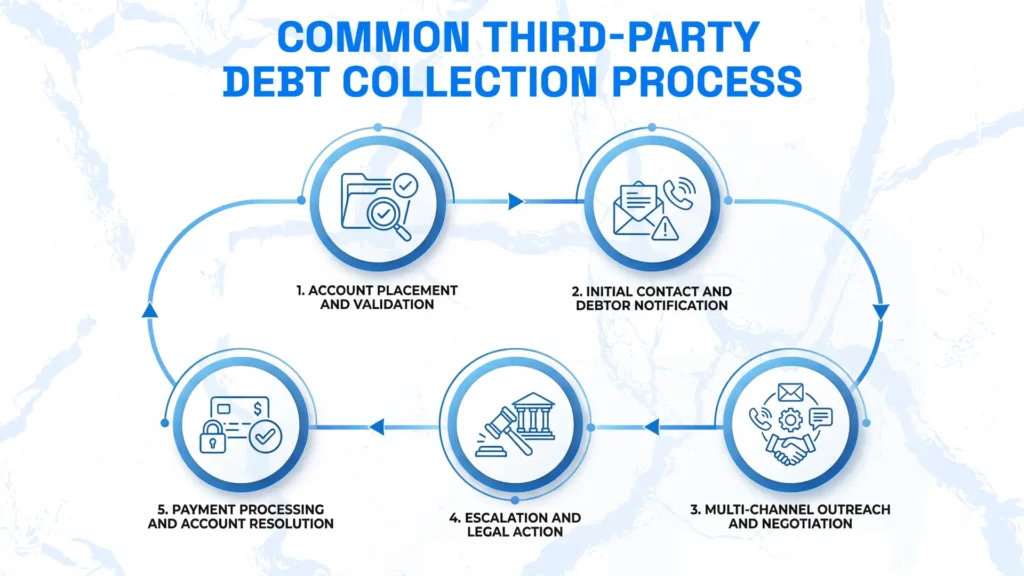

Common Third-Party Debt Collection Process

The debt collection recovery process is data-driven, relying on the accuracy and detail of data to ensure maximum recovery. There are several key stages, and each phase has its regulatory and compliance parameters.

Modern third-party collections operate as a closed-loop system, not a linear handoff. Errors early in the lifecycle compound downstream, affecting contact rates, compliance exposure, and liquidation curves.

For both modern and traditional debt collection process optimization, there are a few standard steps that should be followed.

Account Placement and Validation

The process begins with account placement, regardless of opting for in-house or third-party collection, and many recovery efforts are set up to fail. Accounts need to be:

- Validated for accuracy and completeness

- Verified for legal collectability

- Classified by balance, age, risk profile, and jurisdiction

Manual placement methods like batch file uploads, spreadsheets, and reconciliations can be prone to errors, which slow down time-to-first-contact, AND increase compliance risk.

Compliance requirements are becoming ever more challenging, and misclassifications can lead to insufficient disclosures, which increases the potential for compliance risk. Incorrect classification can trigger FDCPA violations, which expose the agency to penalties as well as delays due to the time needed to rework the data.

Every day lost to reworking data delays first contact, which materially shifts the liquidation curve, especially for aging portfolios. This is why agencies with modern AI debt collection systems require ‘machine-readable precision’ with explicit field definitions.

From our experience, the ideal start off is to have a centralized onboarding portal with a single source of data. This ensures:

- Real-time syncing from creditor systems

- Standardized data formats

- Automated checks for missing or conflicting information

Platforms like Kompato AI enable seamless API-based placement, eliminating batch delays and ensuring every account enters the collection workflow clean, compliant, and ready for action.

Initial Contact and Debtor Notification

Once accounts are validated, agencies must issue legally compliant debtor notifications. This step is tightly regulated and highly scrutinized. Validation notice delivery has strong channel preferences driven by compliance requirements, not consumer preferences.

Requirements typically include:

- Debt validation notices

- Clear disclosure of creditor identity and balances

- Instructions for dispute or resolution

Email is the dominant mode for validation notices, as 5 out of 6 clients explicitly prohibit text delivery. Debt buyers usually hold paper for up to 90 days for the validation period to expire before active collection. This creates a significant timing constraint that affects liquidation curve projections.

Errors like incorrect wording, improper timing, or missing disclosures can trigger FDCPA violations and regulatory complaints.

Modern collection systems automate this entire process by:

- Generating jurisdiction-specific templates

- Enforcing timing rules automatically

- Logging every communication for audit purposes

This ensures compliance is built into the workflow rather than enforced through after-the-fact reviews. Agencies that don’t model validation timing correctly often misattribute weak early performance to portfolio quality, when the real issue is delayed activation.

Multi-Channel Outreach and Negotiation

The legal process for debt collection is omnichannel by design, involving a mix of phone calls, emails, SMS, and secure digital self-service portals to connect with debtors to try to secure payment. This is the most critical phase of third-party debt collection, where most recovery gains or losses are decided. This is also where most traditional models fall short.

Legacy agencies rely heavily on phone calls, and this is a critical bottleneck. Under 1% contact rates are common with tertiary/older accounts due to data decay with declining answer rates and rising TCPA risk.

AI continuously optimizes:

- Which channel to use

- When to initiate contact

- How frequently to follow up

- What messaging or settlement options to present

Rather than using the static scripts of traditional approaches, adaptive models like Kompato AI tailor outreach based on debtor behavior, responsiveness, and payment capacity. The model accesses historical conversations across ALL channels instantly during any interaction. This proves to be more effective than the traditional siloed operations of channels, which require consumers to repeat information.

The advantage Kompato AI’s omnichannel contextual continuity offers isn’t just automation but the ability to reference the full behavioral history across channels instantly, something human collectors simply can’t do at scale. This improves engagement significantly while reducing unnecessary pressure and compliance exposure, while improving consumer experience and collector effectiveness.

Escalation and Legal Action

The next step in the debt collection recovery process occurs when third-party debt collection agencies escalate accounts to legal action after standard omnichannel recovery fails to produce payment, usually within 90 days. This typically involves moving from voluntary repayment negotiations to formal legal proceedings to obtain a court judgment, which could be wage garnishment or asset seizure.

Not all accounts should be escalated, and escalating the wrong accounts can be expensive. Account age affects viable collection channels, and capacity planning should be done accordingly.

Modern agencies apply predictive analytics to determine:

- Which accounts justify escalation

- When the recovery probability no longer supports additional effort

This is important as escalating the wrong accounts will not only reduce ROI but also permanently damage recovery economics through legal fees, complaints, and brand erosion.

End-to-end debt collection tools like Kompato AI protect margins by preventing negative ROI escalation and helping to contain brand risk. It helps prevent wasted legal spend, reduces consumer friction, and protects creditor reputation.

Payment Processing and Account Resolution

The debt collection process comes full circle with the debtors being presented with dynamic, AI-driven offers based on intent, affordability, and risk, allowing consumers to self-resolve without friction.

Debt collection services need to address simple housekeeping issues like accounts getting stuck, skip trace difficulties, and payment processing before winning access to higher-value paper. Payment processing reliability is the gateway to earning more placements and administrative failures block growth.

When a debtor resolves an account, speed and transparency matter.

Kompato AI addressed the needs of the modern debt collection process by integrating the payment processing directly into the collection workflow, enabling:

- Instant payment confirmation

- Automated account status updates

- Real-time remittance reporting

For finance and operations teams, this visibility is critical for accurate forecasting and performance evaluation. For many creditors, real-time finance visibility is the gating factor in expanding wallet share and not the process of debt collection.

What Does Third-Party Debt Collection Cost?

Different clients have different comfort levels with performance-based or fixed-cost pricing. The pricing model preference usually varies by pricing model and the age or complexity of the debt, as well as by client operational practices and overall market economics.

Understanding client accounting and operational preferences helps to structure pricing conversations, and managers need to realize that the selected cost structure has a direct impact on recovery outcomes and long-term ROI.

However, in our opinion, pricing models don’t determine outcomes; the cost per dollar collected does. The right model is the one that aligns incentives, scales efficiently, and preserves compliance margin.

Contingency Fee Arrangements

Contingency pricing is a common model in which agencies retain a percentage of recovered funds.

Typical retention ranges:

- 20%–50%, depending on debt age, volume, and complexity.

However, while this model appears low-risk, it creates hidden inefficiencies due to:

- Agencies prioritizing high-balance accounts

- Lower-balance or complex accounts receiving minimal effort

- Creditors lack insight into effort allocation

High contingency rates also inflate the cost per dollar collected, especially when recovery rates plateau. Pricing negotiation is usually a portfolio-level strategic decision, not just a rate discussion.

In our experience, some key factors that impact our clients’ decision-making process are:

- Discounts for secondary paper can secure 100% of the volume and prevent the client from engaging other agencies.

- Volume drives margin:

exclusive placement = discount.

competitive placement = higher rates (30-32% range)

- 2% liquidation rate is a conservative assumption for forecasting, even though actual rates vary significantly by portfolio age and quality

Flat Fee and Hybrid Models

Currently, flat-fee and hybrid pricing models are gaining traction among more technology-enabled agencies. Debt collection agency processes that opt for offshore labor arbitrage can create pricing pressure that technology can overcome with a performance lift.

While labor cost in low-cost offshore locations like the Philippines can be as low as 22 cents per audio minute, the challenge is to ensure profit and scalability. This is where AI-powered systems have an edge in the debt collection process optimization to price competitively against low-cost labor.

These tools for automating the debt collection process reduce marginal collection costs, enabling agencies to work large portfolios efficiently without proportional increases in headcount. They can deliver performance lift that justifies higher per-account economics.

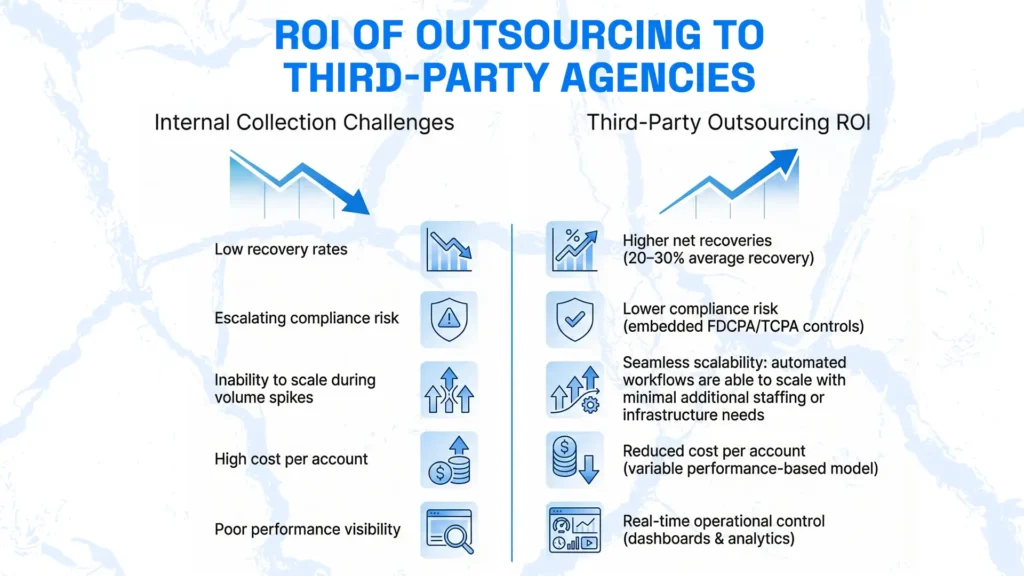

What’s the Real ROI of Outsourcing to Third-Party Agencies?

Outsourcing to third-party debt collectors isn’t just about shifting the load off internal teams; it’s more about measurable performance improvement, cost efficiency, and risk management.

The need for specialized partners is underscored by industry benchmarks showing that third-party collectors return roughly $90 billion to creditors annually, according to Gitnux, while average recovery rates on delinquent accounts sit around 20% industry-wide.

Organizations typically turn to third-party collections to solve five core problems:

- Low recovery rates with internal collections

- Escalating compliance risk

- Inability to scale during volume spikes

- High cost per account

- Poor performance visibility

The modern debt collection process steps address all five by delivering:

- Higher net recoveries: Professional collectors are equipped with persistent outreach workflows and often achieve industry average recovery rates of 20 %–30 % or more, outperforming ad-hoc internal efforts.

- Lower compliance risk: Dedicated agencies embed regulatory requirements into their operations, reducing costly FDCPA/TCPA violations.

- Seamless scalability: automated workflows are able to scale with minimal additional staffing or infrastructure needs.

- Reduced cost per account: Outsourcing shifts fixed internal costs to variable, performance-linked expenses.

- Real-time operational control: Third-party systems often provide dashboards and analytics, enabling creditors to monitor results and adjust strategies quickly.

The result is sustainable, scalable recovery performance that does not trade off short-term gains with long-term risk. Unlike earlier channel innovations, Kompato AI changes decision-making itself, not just the communication medium. The ROI of tools for automating the debt collection process compounds over time.

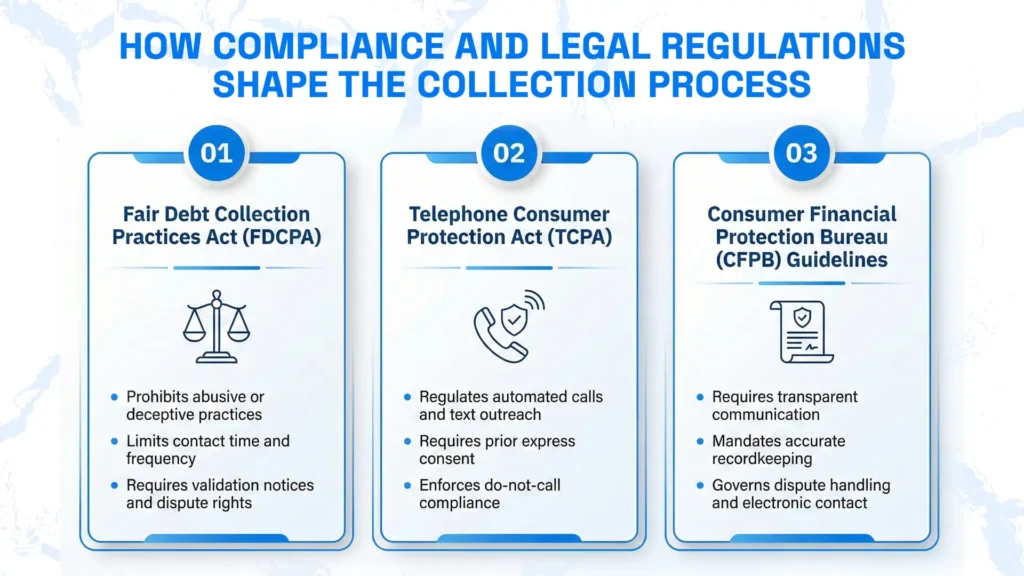

How Compliance and Legal Regulations Shape the Collection Process

Compliance isn’t just a legal requirement; it’s the operating framework that enables trust, scalability, and competitive differentiation. Compliance failures are asymmetrically expensive, and for the mid-market buyers, compliance confidence often outweighs marginal recovery gains.

Compliance concerns are usually based on perceived or experienced regulatory risk about future precedents, not actual current violations.

Fair Debt Collection Practices Act (FDCPA)

This primary federal statute governs how third-party collectors communicate with consumers. It prohibits abusive, harassing, deceptive, and unfair practices, limits contact times and frequency, and requires collectors to provide clear validation notices with debt details and dispute rights.

Telephone Consumer Protection Act (TCPA)

This act regulates automated outreach like autodialed and prerecorded calls and text messages. Debt collectors must obtain prior express consent before contacting wireless numbers with automated communications and honor any do-not-call requests. TCPA breaches can result in significant penalties, making consent and consent-tracking essential compliance components.

Consumer Financial Protection Bureau (CFPB) Guidelines

CFPB guidelines further clarify collector obligations and interpret FDCPA and Regulation F requirements, emphasizing transparent, respectful communications, accurate recordkeeping, and appropriate responses to consumer disputes. The CFPB’s Debt Collection Rule also specifies how electronic communications should be handled and prohibits practices that could harass or mislead consumers.

State-Specific Laws

Many states impose requirements stricter than federal law, like additional disclosure mandates, communication restrictions, licensing rules, and enforcement mechanisms. Agencies collecting across multiple states must align with both federal standards and the varying state-level protections to avoid penalties and legal risk.

How AI Ensures Compliance Automatically

Modern platforms like Kompato AI are the best tools for debt collection process automation as they embed compliance requirements directly into the workflow by:

- Enforcing mandated contact limits in real time

- Tracking consent dynamically

- Adjusting messaging by jurisdiction

- Maintaining complete audit trails

- Flagging risky behavior before violations occur

How Modern Technology Is Transforming Third-Party Collections

From account placement to documentation and reporting, leading agencies rely on platforms that integrate seamlessly with creditor systems. Without real-time reporting, even high-performing agencies operate on lagging indicators, making optimization feel reactive instead of continuous.

Kompato AI is one of the best tools for debt collection process automation with its strong real-time account synchronization features.

Omnichannel Debtor Outreach

AI determines the optimal channel and timing for each debtor interaction, working to maximise engagement while minimizing intrusion and risk.

Adaptive Negotiation and Settlement

Settlement strategies evolve dynamically based on debtor behavior, improving resolution rates without escalating pressure.

Payment Processing and Remittance

Integrated payment workflows accelerate resolution and provide creditors with real-time visibility into cash flow.

Successful debt collection cycle stages now use AI to determine the right channel at the right time, maximizing contact rates while minimizing compliance risk.

Knowing When to Escalate to Third-Party Collections

Escalation to third-party collections is needed when internal recovery efforts reach diminishing returns. At this stage, internal recovery costs outweigh the anticipated returns, compliance risk is rising, and delinquency levels surpass policy thresholds.

Key escalation triggers are aging curves, liquidation benchmarks, and cost-per-dollar collected thresholds.

As marginal recovery rates decline and cost per dollar collected increases, shifting accounts to a contingency-based agency model converts fixed costs into variable, performance-linked expenses while preserving net recoveries and improving forecast accuracy.

Agencies follow strict regulatory requirements, maintain dispute tracking, honor contact limitations, and ensure audit-ready documentation. A poorly managed handoff can create regulatory penalties and reputational risk for both parties.

How to Select and Manage Third-Party Collection Partners

All clients in the market for debt collection services need to do their due diligence, and agencies also need to do their own due diligence to assess portfolio overlap. This can be a major cost and time investment for BOTH parties and can prove to be a key bottleneck.

Onboarding a new agency for debt collection services can create a processing bottleneck for mid-sized debt buyers. It also becomes a significant cost head as the typical onboarding can take over 90 days.

Selecting a debt collection agency process has significant switching costs and should be a cautious investment choice. Kompato AI focuses on reducing switching costs and onboarding friction by standardizing integrations, compliance controls, and reports across agency partners.

Evaluation Criteria Beyond Recovery Rates

We have learnt from working with multiple clients that the best questions to ask are: What fields do they require? What field definitions are negotiable and what are mandatory? Key considerations include:

- Compliance infrastructure

- Technology capabilities

- Transparency and reporting

- Scalability under stress

- Consumer treatment standards

The complexity of the data file format is a primary determinant of onboarding speed. Simple file formats enable rapid onboarding, while complex formats will lead to delays.

Technology and Integration Requirements

Questions to ask about technology and integration requirements are mainly data-centric:

- Do they support API-based integration?

- Is it reporting real-time?

- How is data secured?

- Can they support omnichannel engagement?

Performance Monitoring and Quality Control

Performance data at scale is the key to shifting partner relationships from “testing” to “scaling.” Performance monitoring isn’t just quality control; it’s the basis for expanding the relationship

Wallet share expansion is a key performance-dependent metric for clients to track: 20-30% initial → 50-75% if outperforming internal agency.

Monitor: liquidation rate, cost per dollar collected, compliance incidents, consumer complaints

Best practices include:

- Regular portfolio reviews

- Compliance audits

- Complaint trend analysis

- Performance benchmarking

How to Scale Your Collections Without Adding Headcount

As receivables portfolios grow and economic cycles tighten, many organizations face a common dilemma: demand for collections increases, but adding headcount isn’t feasible or cost-effective. Traditional scaling, hiring more agents to handle more accounts, quickly becomes a bottleneck, driving up costs and inconsistency due to training lags and turnover.

In our experience, manual agencies deal with agent capacity as a hard constraint. Staffing determines what you address, and other heads remain unattended. AI doesn’t just scale the debt collection cycle. It changes what “capacity planning” means entirely by converting dormant receivables into addressable portfolios.

Consider a company with 80-100 agents for 0-90 day collections, but it is sitting on $1.2B of old charge-offs that have never been touched due to manpower constraints.

The Traditional Scaling Problem

Legacy agencies scale by hiring more collectors, which drives up costs and inconsistency. Most in-house and offshore labor teams struggle with any level of volume spikes, whether it is 2x or 10x.

AI can replace a significant agent headcount while maintaining or improving performance. It also helps to eliminate the lag time associated with hiring and training manual heads, as well as removing attrition risk, and ensures lower fixed costs during low-volume periods.

How Modern Agencies Handle Volume Fluctuations

Technology-first agencies scale through automation and AI, enabling rapid volume changes without operational strain. The debt collection process optimization relies on AI-powered systems that scale instantly. No ramp-up time, no quality degradation.

We have experienced with most of our clients that automating omnichannel outreach offers infinite capacity through the best tools curated for debt collection process automation. AI-powered agencies can handle 10x volume overnight without hiring a single additional collector, which is a capability that fundamentally changes capacity planning for debt buyers.

The only realistic scaling bottleneck for the modern debt collection recovery process is email warm-up time, not technology capacity. While digital channels have different scaling constraints than voice agent scaling, they can work through the entire debt collection portfolio, not just what staff capacity allows.

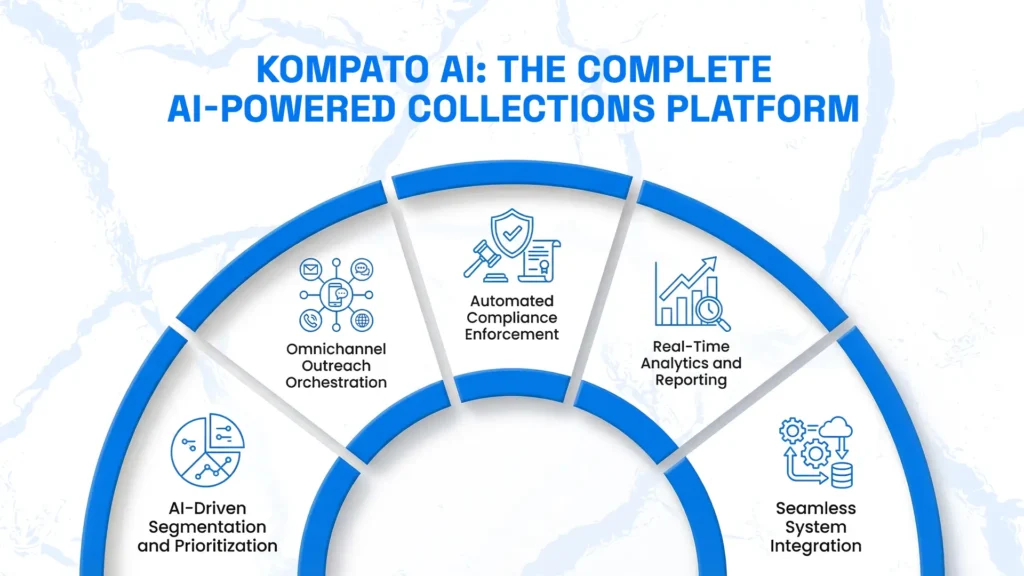

Kompato AI: The Complete AI-Powered Collections Platform

Instead of forcing businesses to choose between automation and agents, Kompato AI operationalizes the entire spectrum from AI-first to human-led, allowing organizations to deploy the optimal mix for their specific portfolio needs. Its AI-first automation handles up to 98% of routine borrower contacts for most portfolios.

Kompato AI is purpose-built for modern collections. It reduces dependency risk for creditors by standardizing tools for automating the debt collection process across agencies. It is designed to support AI-first, human-led, and hybrid operating models within a single orchestration layer.

Standard operations follow a specific channel escalation sequence that starts from emails, moves to triggered phone calls, then texts triggered by call interactions, with the ultimate goal of offering self-service.

It provides:

- AI-driven segmentation and prioritization

- Omnichannel outreach orchestration

- Automated compliance enforcement

- Real-time analytics and reporting

- Seamless system integration

Kompato AI doesn’t replace agencies; it powers the process of debt collection, enabling creditors to demand better outcomes at lower risk and cost. Kompato AI’s performance stems from architectural separation, real-time controls, and continuous monitoring, rather than reliance on post-hoc review alone. It is the operating system for the debt collection process optimization.

Building Your Modern Third-Party Collections Strategy – Final Thoughts

Our insights into third-party collections show that they are no longer about outsourcing effort; they’re about offering optimized AI tools for automating the debt collection process. The most effective programs embed compliance parameters into workflows, use AI to personalize engagement at scale, demand transparency from partners, and measure ROI holistically to drive continuous improvement.

This approach transforms collections from a cost center into a scalable, compliant growth function. Platforms like Kompato AI combine automation, real-time analytics, and decision intelligence to enhance recovery outcomes, preserve customer relationships, and reduce risk, making system-driven collections a competitive advantage for modern businesses. Feel free to reach out to us to see how Kompato AI can help refine your collections strategy.

Frequently Asked Questions

Typically between 60–120 days delinquent, guided by behavioral and risk data rather than fixed timelines.

Most recoveries occur within the first 30–60 days, especially when AI-driven prioritization is used.

API integration, omnichannel outreach, automated compliance controls, and real-time reporting are baseline expectations.

Most consumer and commercial debts are eligible, though legal requirements may vary by jurisdiction and debt class.