Getting a loan today shouldn’t feel like applying for one a decade ago. Consumers now expect the process to take just a few clicks, with instant approvals, transparent terms, and a personalized experience. No paperwork or branch visits.

At the same time, lenders are under pressure to recover more with less while being fully compliant with rising delinquency volumes.

Many lenders still operate on legacy systems, manual underwriting, fragmented tools, and one-size-fits-all strategies, which don’t fulfill consumers’ expectations and their own goals.

Artificial intelligence is emerging as the structural response to these pressures. The AI in the lending market is projected to grow from $11.63 billion in 2025 to $14.71 billion in 2026. It’s already influencing KPIs like approval speed, cost-to-originate, liquidation rates, servicing efficiency, agent productivity, and customer experience across the lending life cycle.

In this article, we provide a deep dive into AI use cases in the lending industry and share an actionable roadmap for embedding it into your operations to stay competitive!

The State of AI Adoption Across the Lending Lifecycle

We have found some interesting insights that signal strong institutional investment and rising operational demand for AI in the lending industry.

- Globally, the AI in the lending market is projected to reach $58 billion by 2033, growing at a 23.5% CAGR.

- According to McKinsey, AI could add $200–$340 billion in annual value to the banking sector across credit decisioning, risk management, and customer engagement.

- Recent surveys highlight that 88% of financial institutions now leverage AI in at least one business function, with 73% of lenders citing operational efficiency as the primary motivation.

Yet, adoption remains fragmented. Roughly two-thirds of institutions are still in early-stage experimentation. What we have observed is that the adoption gap is more psychological than technological. Compliance anxiety and organizational inertia create a “fear gap,” meaning “there’s more fear about making the wrong move than excitement to make the right move”.

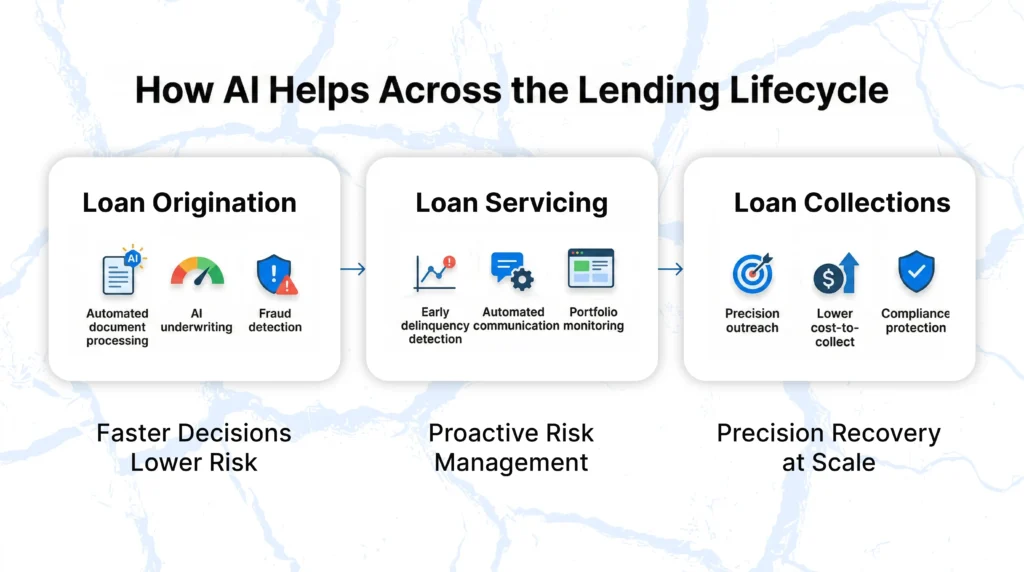

AI in Loan Origination — Faster Decisions, Lower Risk

Loan origination marks the beginning of the borrower’s journey. Traditionally, this process was highly manual, which resulted in delays, inconsistencies, fraud attempts, and missed opportunities.

With AI in loan origination, decision times have dropped from days to minutes, manual reviews are automated, and approval consistency has improved.

While AI in loan origination has moved well beyond pilot programs, most implementations exist in silos. The real competitive advantage comes from connecting origination data to downstream stages.

Automated Document Processing and Data Extraction

Human errors in data entry or document review can lead to costly delays. One of the most critical AI use cases in lending is the AI-powered document processing that replaces the document-intensive lending process with a fast, automated, and accurate digital workflow. We have found that AI delivers 99% accuracy in data extraction (with 1% human-in-the-loop for exceptions) and 3x+ decrease in loan cycle time.

Leveraging computer vision and natural language models in an AI lending platform, lenders can extract data from diverse documents like income details, bank statements, pay stubs, and tax forms. OCRs in AI-based lending platforms can even recognize and extract data from low-quality files (scanned copies, photos, and handwritten forms), verify every field, flag duplicates, and detect incomplete or suspicious inputs.

Most importantly, with AI in loan processing, lenders capture structured data accurately at origination, which creates a reliable borrower profile. When further standardized and integrated using AI techniques, this information creates a strong foundation for ongoing risk monitoring and servicing personalization.

AI-Driven Credit Scoring and Underwriting

Traditional underwriting models rely on static scoring and do not adapt well to unique borrower profiles. According to Neontri, AI credit rating systems continuously learn from diverse data signals and improve risk assessment accuracy by 15–25% and reduce default rates by up to 30%.

Modern AI underwriting models evaluate thousands of variables beyond traditional credit scores, such as transaction patterns, cash flow consistency, repayment behavior, and current financial situations, and generate a scorecard.

Lenders can leverage these real-time insights in their AI-based lending platforms to make more informed, data-driven decisions to improve their portfolio performance and customer experience. A few AI use cases in lending at the loan origination phase include:

- Confidently approving creditworthy thin-file applicants

- Reducing false declines

- Adjusting credit limits dynamically

- Refining risk-based pricing

- Personalizing repayment terms

- Detecting early signs of default

However, if underwriting intelligence remains isolated, lenders miss predictive advantages that extend well beyond day-one approval. Also, it’s important to note that ML-based underwriting models require explainable AI (XAI) principles to satisfy regulatory review.

Another key point to note is that AI credit scoring models learn from historical data, which can unintentionally carry forward existing biases if not carefully managed. Without proper oversight, this may impact fair lending outcomes.

Using diverse datasets, transparent modeling, data balancing techniques, and rigorous bias testing ensures more equitable, compliant, and responsible AI-driven credit decisions.

Fraud Detection During Origination

An average American bank faces 24,000 fraud attacks yearly. AI anomaly detection catches what manual review misses. Machine learning algorithms shift teams from reactive, rule-based systems to proactive, real-time solutions.

The U.S. Department of the Treasury recovered over $375 million in fiscal year 2023 via enhanced AI fraud detection. As of 2025, 91% of U.S. banks use AI for fraud detection.

For example, when a borrower applies for a loan, an AI lending platform can automatically detect anomalies in identity data, document tampering, device fingerprints, synthetic identities, and loan stacking in real time and generate fraud scores.

Lenders use fraud scores to measure the legitimacy of a transaction before funds are disbursed. The best implementations layer fraud detection with risk-tiered verification rather than one-size-fits-all scrutiny

AI in Loan Servicing — Proactive Management That Prevents Defaults

Loan servicing is where lender profitability is either protected or lost. After origination, the challenge shifts from assessing risk to managing it in real time. In this middle stage, servicing AI acts as the bridge between origination and collections.

Servicing is where the “data silo” problem becomes most acute. Origination data, payment behavior, communication history, and external signals must all be unified for servicing AI to work efficiently.

Predictive Analytics for Early Delinquency Detection

Traditionally, servicing has been reactive: lenders respond after a debtor misses a payment, declares hardship, or delinquency escalates.

With AI in lending, models analyze repayment behavior, transaction trends, payment timing shifts, and external economic signals to detect early signs of borrower stress.

Imagine a scenario where transaction data shows recurring overdraft fees over two months. AI lending platform identifies financial stress and offers a short-term hardship plan instead of aggressive outreach. As a result, the borrower enrolls before delinquency occurs, and lenders also maintain customer trust.

Preventing delinquency is significantly more cost-effective than recovering from it. That’s why predictive servicing reduces loan delinquencies by 25% while preserving customer relationships.

However, predictive models are only as good as their data inputs. Most lenders lack a framework to measure which data sources actually predict delinquency.

Automated Borrower Communication and Self-Service

The servicing stage involves high volumes of routine interactions such as balance inquiries, payment confirmations, due-date changes, and plan adjustments. AI-powered communication platforms serve multiple AI use cases in lending, like streamlining workflows through intelligent chatbots, SMS campaigns, email automation, IVR systems, and borrower self-service portals.

For example, agentic AI in lending can proactively remind a borrower of an upcoming due date, suggest alternative payment plans if early delinquency risk is detected, or offer a one-click option to enroll in autopay, all within a secure digital channel.

AI lending automation not only reduces call center dependency but also improves borrower experience. Organizations deploying AI-powered virtual assistants and intelligent outreach can cut operational costs up to 40% and increase customer satisfaction 30%.

Customers can reschedule payments, update contact details, or enroll in autopay 24/7 without waiting for a human agent. Human agents then act as a scarce resource to resolve complex or sensitive cases that require a higher level of empathy and judgment.

It’s important to consider that effective self-service requires unified memory across channels; otherwise, automated outreach becomes repetitive and damages borrower experience. Plus, self-service portals also need payment processor integration, multi-path payment routing (ACH, card, etc.), and verification APIs.

Portfolio Monitoring and Risk Intelligence

AI in the lending industry enables real-time, 360-degree visibility into debt portfolios, moving beyond static spreadsheets to dynamic, actionable dashboards. AI-based lending strategies continuously evaluate loan performance, segment trends, compliance monitoring, automated exception flagging, geographic risk shifts, and behavioral clusters.

AI in loan servicing supports proactive policy adjustments like tightening underwriting in emerging high-risk segments, adjusting line management strategies, or reallocating servicing resources toward vulnerable cohorts. Portfolio-wide insight transforms servicing from administrative oversight into strategic risk management.

Suppose a geographic risk model flags growing financial stress in areas affected by layoffs in a major industry. AI lending platform reallocates servicing resources to those accounts and offers flexible repayment options.

Why AI in Collections Is the Biggest Untapped Opportunity for Lenders

Collections are where lending economics are ultimately decided. Approval speed, servicing efficiency, and customer acquisition all matter, but recovery performance is the key that determines portfolio profitability.

Yet AI in debt collection remains one of the least modernized areas of the lending lifecycle, despite the highest number of its AI use cases in lending. The future of AI debt collection is far beyond just automation. It is about precision, timing, and strategy optimization that directly impacts business KPIs, including liquidation rates, promise-to-pay rates, recovery velocity, compliance control, and long-term borrower relationships.

Moving From Volume-Based Outreach to Precision Recovery

Traditionally, lenders often prioritized volume-based outreach. More calls, more emails, more attempts with one-size-fits-all strategies. Rather than recovering more, they increased operational strain without guaranteeing better outcomes. In many cases, over-contacting leads to disengagement, complaints, or regulatory risk.

Compared to traditional debt collection approaches, with AI in the lending industry, collection operators now leverage account-level strategy selection that improves liquidation rates while reducing wasted outreach effort.

By analyzing payment history, behavioral signals, hardship indicators, and prior engagement data, models can predict the likelihood of repayment, optimal contact timing, and appropriate repayment structures. We have observed that these successful debt collection strategies boost recovery rates while adhering to compliance requirements.

So instead of applying uniform pressure, lenders can match strategy to borrower profile, like:

- Soft-touch engagement for short-term liquidity issues

- Structured plans for sustained hardship

- Accelerated recovery for high-capacity payers.

Reducing Cost-to-Collect While Increasing Agent Productivity

Traditional collections scale by adding agents and dialer capacity. Labor represents the largest expense, yet agent turnover remains high, and performance varies widely. Agentic AI in lending acts as an intelligent resource that assists human agents without replacing them by handling routine inquiries and initial contacts, which cuts collection costs by 50%.

Human agents then focus on high-risk accounts that require careful judgment, empathy, or escalation. This results in higher right-party contact rates, shorter resolution cycles, and improved productivity per agent without expanding headcount.

What we have observed is unlike traditional approaches, where human resources and cost scale linearly with rising delinquency, tools like Kompato AI handle spikes without a proportional increase in cost. At Kompato, we have scaled from 10K to 1M+ accounts in 45 days.

Strengthening Compliance and Protecting Brand Reputation

Regulatory scrutiny in collections continues to intensify in 2026. Over-contacting, inconsistent disclosures, and improper documentation expose lenders to financial penalties and reputational damage. At scale, manual processes make consistent enforcement difficult.

AI-powered systems like Kompato AI embed compliance rules (FSCPA, TCPA, Regulations F, state-level requirements) directly into communication workflows through “Compliance-as-code”. Now the system automatically controls frequency caps, channel permissions, consent tracking, and message consistency across all channels through omnichannel communication.

Beyond compliance, automated debt collection techniques also improve borrower experience through respectful, timely, and context-aware engagement that preserves customer trust and brand reputation. Companies with extremely strong omnichannel customer engagement retain, on average, 89% of their customers, compared to 33% for companies with weak omnichannel customer engagement.

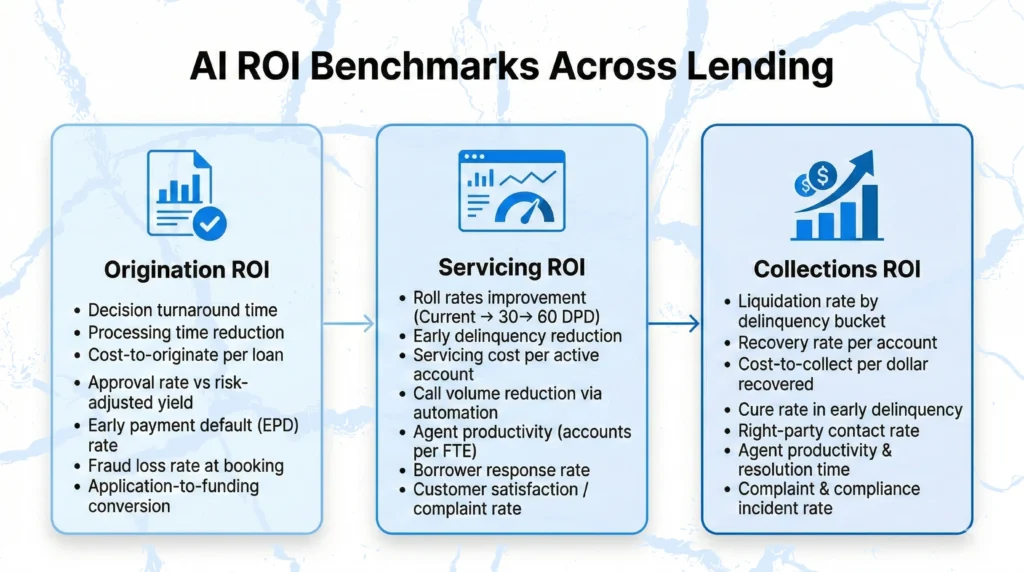

Measuring ROI Across the AI-Powered Lending Lifecycle

Lenders must define stage-specific benchmarks across origination, servicing, and collections to measure the ROI before implementing AI in lending. Each phase has distinct performance drivers, cost structures, and risk dynamics. Also, ROI timelines differ by stage: origination AI shows results in weeks, servicing AI in months, collections AI in 3-6 months (due to compounding data effects)

However, performance benchmarks are meaningful only when measured against proper baselines. CFOs and revenue leaders should use a structured champion/challenger methodology with clearly defined control groups to isolate AI impact from external variables such as seasonality, portfolio mix shifts, or macroeconomic changes.

Below, we recommend the primary ROI benchmarks CFOs and revenue leaders should monitor at each stage of the AI-powered lending lifecycle:

Origination ROI Benchmarks

A strong AI implementation in this phase should reduce processing costs, maintain or improve credit quality, lower early-stage losses, and increase funded volume without proportionally increasing cost.

We highly recommend that origination AI should generate data that feeds downstream stages for greater compounding value because connected-stage ROI is way better than stand-alone stage ROI.

Origination ROI is typically measured across five dimensions: speed, cost, risk, quality, and conversion.

Key benchmarks include:

- Decision turnaround time (minutes/hours vs. days)

- Processing time reduction

- Cost-to-originate per loan

- Approval rate vs. risk-adjusted yield

- Early payment default (EPD) rates

- Fraud loss rate at booking

- Application-to-funding conversion rate

Servicing ROI Benchmarks

Effective AI in servicing should demonstrate measurable reductions in early roll rates while lowering per-account servicing costs. Servicing ROI focuses on delinquency prevention and operational efficiency.

Core benchmarks include:

- Roll rates (current → 30 DPD, 30 → 60 DPD)

- Early-stage delinquency rate reduction

- Servicing cost per active account

- Call volume reduction through automation

- Agent productivity (accounts handled per FTE)

- Borrower response rate

- Customer satisfaction or complaint rates

Collections ROI Benchmarks

Collections ROI is the most direct financial metric. Benchmarks should track both recovery performance and efficiency. A successful AI deployment in collections should increase recoveries, shorten resolution cycles, reduce cost-to-collect, and strengthen compliance control simultaneously.

Critical metrics include:

- Liquidation rate by delinquency bucket

- Recovery rate per account

- Cost-to-collect (per dollar recovered)

- Cure rate in early-stage delinquency

- Right-party contact rate

- Agent productivity and resolution time

- Complaint and compliance incident rates

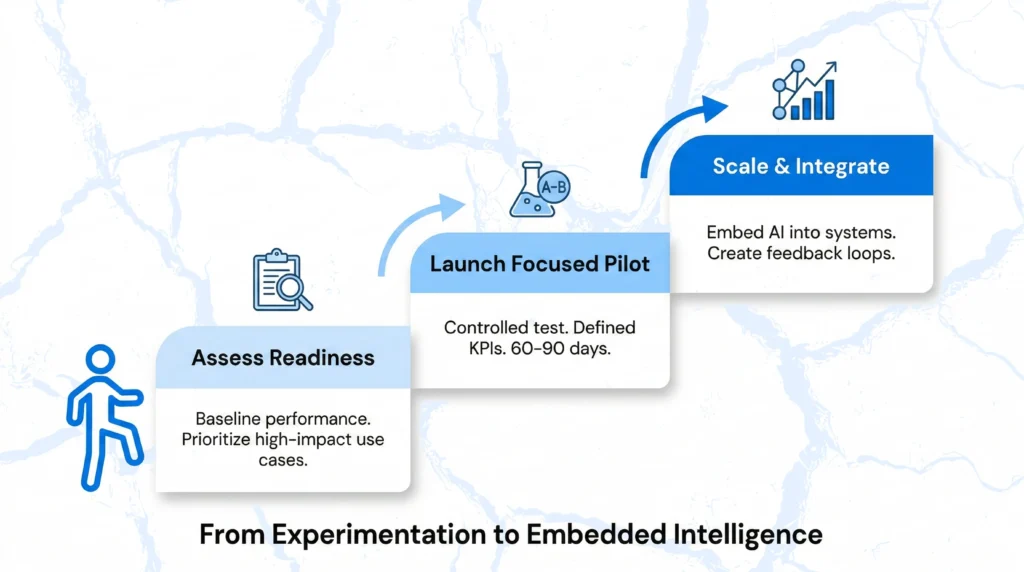

A Practical Roadmap for AI Implementation in Lending

Instead of treating AI as a technology experiment, the most successful leaders treat AI implementation as a structured rollout tied to measurable business outcomes. We have observed that the biggest practical barrier isn’t technology selection, it’s internal organizational readiness and integration complexity.

Based on our years of experience in this industry, we provide an actionable step-by-step roadmap to implement AI in lending operations below:

Phase 1 — Assess and Prioritize

Start by mapping your current lending operations across origination, servicing, and collections. Identify the highest-friction, highest-cost AI use cases in lending operations that deliver quick wins. This requires establishing clean baselines as discussed above before introducing any AI layer.

The objective in this phase is focus: select one or two AI use cases in lending with the highest financial upside and operational feasibility, rather than launching multiple fragmented initiatives. For most lenders, collections will be the highest-ROI starting point because of the lowest current AI adoption (18%), the highest margin impact, and the lowest-risk pilot options.

After identification, rank opportunities based on financial impact and implementation feasibility.

For example:

- If underwriting false declines are high, AI credit decisioning may offer an immediate revenue lift.

- If collection costs are rising, predictive prioritization or automated outreach may deliver faster ROI.

Phase 2 — Start with a Focused Pilot

Once priorities are clear, implementation should begin with a tightly controlled pilot using a champion/challenger framework and a clearly defined control group. The most effective starting point is an integration-light proof of value approach. Instead of waiting 6–12 months for deep IT integration, lenders can leverage third-party APIs or managed service models that layer onto existing workflows without re-architecting core systems.

- A minimum viable pilot design should be tightly scoped. For example, apply AI to accounts in the 90–120 days past due (DPD) bucket or a tertiary placement segment.

- Define 3–4 measurable KPIs upfront, such as liquidation rate, cost-per-dollar-collected, right-party contact (RPC) rate, compliance incidents, and consumer satisfaction.

- Run the pilot for 60–90 days using a champion/challenger methodology with a clearly defined control group.

The purpose of the pilot is to validate business impact, not to prove that AI “works.” A focused pilot also reveals integration challenges, compliance gaps, or workflow friction before full-scale deployment.

Phase 3 — Scale and Optimize

After a measurable impact is proven, scaling should be gradual and operationally embedded. AI outputs must integrate directly into lending systems so that insights influence business decisions rather than sitting in parallel reports.

Effective scaling requires a phased data strategy.

- First, unify data within each stage to establish a clean, reliable source of truth.

- Second, build cross-stage reporting to enable visibility across the lending lifecycle.

- Third, implement automated feedback loops where model outcomes continuously inform upstream decision-making.

For example, a lender that successfully pilots predictive delinquency detection in personal loans may expand it across auto loans and small business portfolios. Over time, dynamic risk dashboards reveal geographic clusters of rising stress. The lender responds by tightening underwriting criteria in specific regions and reallocating servicing teams to higher-risk cohorts before delinquency escalates.

The Future of AI-Powered Lending

AI in the lending industry is moving beyond isolated automation use cases toward fully adaptive, intelligence-driven ecosystems. The next phase will redefine how lenders price risk, allocate capital, personalize borrower engagement, and manage portfolios in real time. Institutions that invest early in scalable AI infrastructure, data harmonization, and model governance will gain competitive advantages in risk precision, operational efficiency, and customer lifetime value.

Looking ahead, we can expect:

- Continuous risk scoring: Real-time borrower monitoring that dynamically adjusts limits, pricing, and servicing strategies, not just periodic risk scoring.

- Autonomous decision engines: AI agents that manage routine credit, servicing, and collections decisions with minimal human intervention.

- Lifecycle intelligence loops: Collect outcomes automatically, feeding underwriting models to improve future originations.

- Hyper-personalized borrower engagement: AI-driven communication tailored to real-time behavioral signals and financial context.

- Regulatory-grade AI governance: Built-in explainability, bias monitoring, and compliance auditing as standard infrastructure, not afterthoughts.

The lenders winning tomorrow are the ones deploying AI across the entire lifecycle today, especially in collections, where the ROI is highest, and the competition is still catching up.

Kompato AI — The AI Collections Platform Built for the Modern Lending Lifecycle

By now, the pattern is clear. Origination has matured. Servicing is evolving. But collections remain the biggest performance lever and the most operationally constrained.

Rising delinquency, tightening compliance, disconnected systems, agent burnout, inconsistent messaging, and escalating cost-to-collect continue to pressure first-party lenders.

Kompato AI is an AI debt collection platform built specifically to solve these modern challenges. Kompato AI serves both first-party lenders and third-party debt buyers, recovering pre-charge-off and post-charge-off accounts, each with maximum recovery targets.

We integrate directly with your existing payment gateway or payment APIs. The borrower experiences the interaction as fully first-party.

- Kompato AI maintains a unified communication memory that tracks every interaction across SMS, email, voice, and digital channels. Operators communicate with full context, ensuring that each engagement builds on prior history.

- We’ve driven liquidation rates 20% higher than those of peer agencies within three months.

- Kompato applies AI-driven segmentation and strategy selection to match engagement style, timing, and repayment options to each borrower profile. Automation handles lower-friction resolutions.

- Human agents focus on situations where their complex and empathetic negotiation drives value. Currently, Kompato’s AI agents resolve 96.4% of queries, and only 3.6% of live voice calls are escalated to humans.

- Our compliance report shows 99.91% pass rate across 45 regulatory (FDCPA, TCPA, and UDAAPs, state-level-requirements) and internal policies.

Conclusion

AI in lending is transforming the whole lending lifecycle from its origination to collection. AI is not a threat to human agents that could replace them; it empowers them. The lenders and agencies that move beyond fragmented tools and manual recovery models will see measurable gains in processing time, higher liquidation rates, cost-to-collect, stronger compliance control, lower default risks, and more personalized borrower experiences.

Kompato AI is built to help first-party lenders modernize collections without operational disruption. If you’re evaluating how to integrate and scale AI in collections responsibly and profitably, now is the time to act.

Ready to transform your debt collection strategy with AI? See how Kompato AI can help you recover more with less. Schedule a demo today!