Debt collection has always been a complex and high-stakes function of the financial system.

But in 2026, it’s facing unprecedented pressure. Delinquency rates are up, borrower behavior has changed, and regulators are more active than ever. Meanwhile, consumers expect frictionless digital experiences, even when behind on payments.

Most collections teams are being asked to do more with less, working across higher volumes, tighter margins, and older tools not built for today’s realities.

At Kompato, we draw on years of experience across AI, compliance, and collections technology. This guide is our strategic perspective on how automated debt collection can enhance recovery rates. We’ll show how the right debt recovery software can boost liquidation, reduce risk, and improve the consumer experience, all while lowering cost.

And we’ll back it up with benchmarks, case studies, and lessons learned from building one of the most advanced automated debt collection platforms in fintech.

The State of Debt Collection in 2026

Debt recovery in 2026 is under pressure from every direction. Consumer balances across credit cards, BNPL, and unsecured loans are climbing, while rising delinquency rates continue to strain traditional recovery models. According to recent data from the Federal Reserve Bank of New York, 4.5% of all outstanding household debt was delinquent as of Q3 2025, pushing recovery teams into volume levels that manual operations simply cannot absorb.

Regulators have taken notice. The CFPB is increasing its scrutiny of contact frequency, communication disclosures, and harassment risks under FDCPA, TCPA, and Regulation F. States like California and New York have added their own oversight layers, raising the bar for compliance. Any slip, be it in a phone call, a text, or a missed notice, can now trigger major consequences.

Borrowers, meanwhile, expect the same level of flexibility and control they get from their banking app. They want to manage payments on their time, through channels they prefer, without pressure.

Most traditional collection shops can’t deliver that.

This is no longer just a technology gap. It’s a structural one. And it’s why more organizations are exploring modern debt collection techniques and turning to automated debt collection software and rethinking how they automate collections at scale.

Why Debt Collection Is Overdue for Transformation

The Limitations of Traditional Collection Approaches

What we have observed is that most traditional collections operations still rely heavily on manual workflows: dialers, spreadsheets, agent-led negotiations, rigid scripts, and fragmented follow-ups. These methods may have been passable in a low-volume and low-regulation world, but they cannot scale.

Human agents are overloaded, trying to personalize outreach across thousands of accounts with incomplete data and no system memory. Debtors face impersonal, frustrating experiences. Leaders are forced to choose between unsustainable headcount growth and stagnant results.

Take a mid-sized lender using spreadsheets and dialers to manage delinquent accounts. Agents juggle dozens of callbacks a day, missing follow-ups or logging incomplete notes. A single misstep, like a missed disclosure, can trigger costly compliance issues.

That’s why we recommend replacing manual and error-prone approaches with a modern automated debt collection system: one that orchestrates outreach, handles negotiations, and ensures compliance across channels. We’ve seen firsthand how tech-driven workflows reduce labor, increase liquidation, and give consumers the digital-first experience they now demand.

Read More: AI Powered Debt Collection vs Traditional Methods

Still, transformation barriers vary. Large institutions have resources but move slowly. Small firms move fast but often lack depth. Mid-sized lenders face the most friction: pressured to modernize, yet risk-averse. External constraints like bank oversight, litigation fears, and regulatory uncertainty often delay change more than internal readiness.

At this point, the question is no longer whether to modernize, but how to automate debt collections without losing control, compliance, or empathy.

Rising Regulatory Pressure on Collection Practices

Regulators have signaled clearly that the old way of doing things won’t fly in a digital world. The CFPB continues to pursue enforcement actions tied to contact frequency, communication disclosures, and harassment allegations. TCPA litigation remains a steady risk for outbound dialing, and Regulation F has formalized a new baseline for consumer contact management.

As we mentioned earlier, state-level rules are also piling on. Even well-meaning teams find it hard to track everything without the help of automation.

We have observed that building compliance into your core workflow is the only sustainable answer. With automated debt collection technology, you can embed legal rules directly into your contact logic. Kompato AI, for example, uses machine-executed safeguards to enforce contact frequency caps, state-by-state licensing filters, and automated disclosures, backed by timestamped logs across every channel.

Consumer Expectations in the Digital Age

Borrowers may be behind on payments, but they’re not behind on technology. They use digital wallets, chat apps, and self-service tools in nearly every aspect of their financial lives. What they expect from collections isn’t special treatment, but a basic level of control, clarity, and respect. They want to resolve issues without waiting on hold or navigating outdated portals. They want answers, not pressure.

This shift is about dignity. Consumers engage more when systems respect their context and offer choices. Traditional collections still feel rigid and one-sided. Today, relevance requires meeting people on their terms, through their preferred channels.

In fact, according to Salesforce, 80% of customers now say the experience a company provides is as important as its products and services, and 73% expect better personalization as technology advances. Yet over half (55%) still feel like they’re interacting with disconnected departments. These expectations don’t change when consumers become borrowers; they expect consistency, control, and empathy from every financial interaction, including collections.

What is Automated Debt Collection and What Does it Look Like

Automated debt collection uses technology to manage recovery workflows end-to-end. With the help of AI,It prioritizes accounts, contacts borrowers, negotiates payment, and ensures compliance, without manual agents. The goal is to deliver speed, consistency, and compliance at scale.

In our experience, the most effective automated debt collection software functions as comprehensive debt recovery software, combining behavioral data, decision logic, and omnichannel communication into one unified platform. Instead of relying on agents to decide who to contact and how, the system applies predictive analysis, machine learning, and predefined business rules to determine the next best action.

Messages are sent automatically via SMS, email, voice, or web portal based on borrower engagement history and communication preferences. Payment plans are negotiated in real time using conversational AI, and every compliance step is documented before, during, and after each interaction.

This is not about replacing humans entirely, but about letting automation handle the repeatable work, while human agents step in where a higher level of empathy, complexity, or judgment is truly needed.

To understand where this balance is heading, explore our take on the future of AI in debt collection.

We think of it as moving from a traditional call center to a digital control tower, where collections technology works intelligently in the background, enabling scale and oversight from day one.

Key Ways Automation Transforms Debt Collection

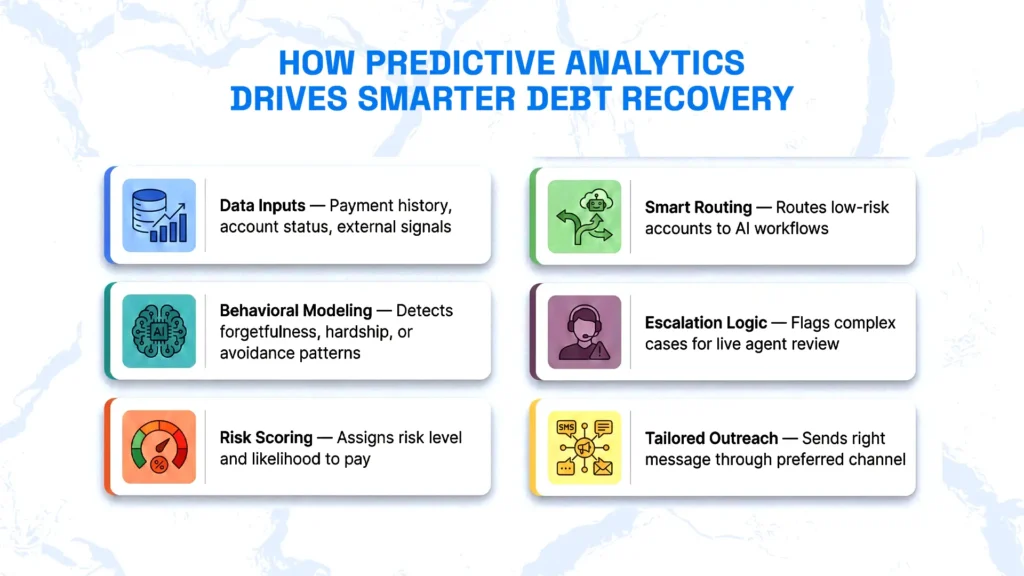

Predictive Analytics and Behavioral Modeling

Modern platforms use payment history, account status, and external signals to predict who’s likely to pay, when, and under what terms. This enables tailored outreach (like whether someone is forgetful, in hardship, or avoiding contact), resulting in high engagement and smarter recovery.

Accounts flagged as lower risk or highly responsive are routed to AI-powered workflows, while complex or high-risk cases are escalated to live agents.

Smarter Account Prioritization and Segmentation

Automation dynamically segments accounts by risk, delinquency age, debt type, vintage, and likelihood to pay to apply tailored strategies for each segment. For example, fresh prime accounts respond very differently from older or out-of-stat paper, and credit card debt behaves differently from fintech loans. Likewise, small balance accounts often require a different strategy than larger ones. This kind of targeted segmentation leads to higher ROI per contact.

This kind of orchestration lets organizations automate collections with precision and lift ROI per contact.

Automated Multi-Channel Outreach

Borrowers expect multi channel outreach across through text, email, voice, and portals. Automation orchestrates this seamlessly.

Fusion reports that text messages have a 98% read rate and 500% higher response rate than email. Missed emails can trigger SMS follow-ups; paused plans can resume via the portal, which reduces friction and improves resolution.

Email and SMS can drive inbound activity by linking to portals or prompting calls, reducing the need for outbound dialing. Email is nearly free; SMS costs ~4¢ per message. Smart channel sequencing improves engagement and lowers cost-per-dollar collected.

Assigning dedicated phone numbers to each channel enables precise attribution, helping teams understand what drives inbound engagement.

Proactive Payment Reminders That Reduce Delinquency

Automation uses behavioral triggers to send reminders at the right moment. For example: nudging younger borrowers via SMS between 6-8 PM when they’re most responsive.

These prompts are tailored, timely, and delivered through preferred channels. One-click resolution links remove friction, making it easier for borrowers to take action and prevent accounts from rolling deeper into delinquency.

Real-Time Negotiation and Dynamic Payment Plans

Conversational AI empowers borrowers to explore options like settlements, deferments, or split payments instantly, without waiting on hold. Plans adjust dynamically based on factors such as income bands, hardship indicators, or prior behavior.

Every interaction is logged automatically to ensure compliance, reduce manual oversight, streamline resolution, and respect individual circumstances.

Self-Service Portals for Debtor-Led Resolution

Many digital-first borrowers prefer resolving debts independently. Self-service portals provide secure, on-demand access to account details, payment options, and documentation.

Portal integration with email and SMS nudges offers convenience and drives resolution to convert passive intent into completed payments without agent intervention.

Smart Escalation to Human Agents

NLP and sentiment analysis detect stress signals like “I just got laid off,” and escalate to human agents. This preserves empathy while avoiding redundant follow-up questions.

To ensure these escalations are handled effectively, the system closely monitors AI-to-agent transfers. Any missed or delayed handoffs are added to a prioritized manual worklist. Built-in time management rules help agents respond promptly, minimizing drop-offs. Since the full conversation history is preserved during the handoff, borrowers don’t have to repeat themselves, thus avoiding confusion, duplicate logs, and rework.

Continuous Compliance Monitoring and Documentation

Automation enforces FDCPA, TCPA, and Regulation F rules within the system logic through Compliance-as-Code.

All interactions are logged with timestamps, creating a reliable audit trail and reducing manual compliance risk.

The ROI Potential of Automated Debt Collections

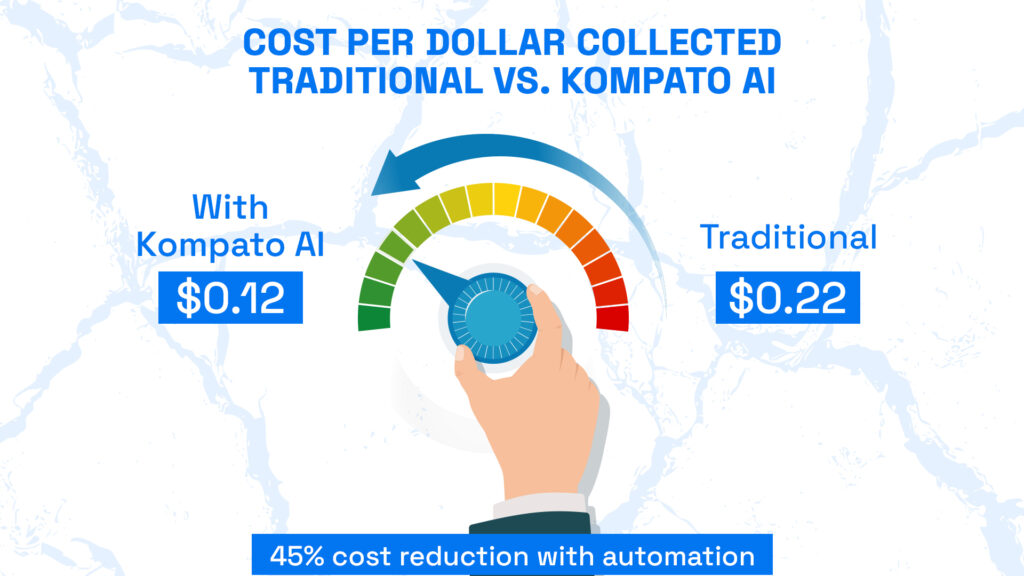

Cost Per Dollar Collected Benchmarks

Traditional collection models come with high fixed costs like high headcount, training, supervision, and infrastructure, even when contact rates decline. Modern debt recovery software, on the other hand, enables leaner operations by offloading outreach, negotiation, and documentation tasks to software that scales instantly.

Automation can reduce operational costs by 40%. In one implementation, Kompato AI brought cost per dollar collected down from $0.22 to $0.12, delivering a 45% cost reduction.

Liquidation Curve Improvements

Beyond cost, automation accelerates collections. By engaging borrowers faster, using behavior-driven logic, and avoiding drop-offs common in manual processes, liquidation timelines shorten, and overall recovery rises.

Kompato’s AI-powered platform improved liquidation by up to 57% across pilot portfolios. In a U.S. challenger test, it outperformed three incumbent agencies by 39% within weeks.

Cash Flow and Portfolio Velocity

Speed matters in collections. Delayed contact reduces recovery probability. Automation makes contact immediate and intelligent, allowing lenders to cycle portfolios faster and improve liquidity.

In one deployment with a U.S.-based subprime consumer lender, Kompato AI complemented AI-driven speed with intelligent segmentation, resulting in an 87% improvement in contact efficiency and RPC rates rising from 35% to 52% over the first 12 weeks. While results vary by segment, this example highlights the potential for rapid lift when automation is paired with behavioral targeting.

Why Better Consumer Experience Drives Better Results

Higher Response and Engagement Rates

In our experience, borrowers are far more likely to engage when automated debt collection feels personalized, timely, and dignified. Generic calls are ignored. But outreach through preferred channels, including SMS, email, or self-service portals, at the right time, using the right tone, drives action.

Improved Promise-to-Pay Conversion

Borrowers rarely object to repayment, but to how it’s presented. Flexible and nonjudgmental communication powered by conversational AI and automated debt collection systems helps them commit without pressure.

Kompato AI allows users to explore dynamic payment plans or hardship deferments on their own, improving PTP conversion without increasing agent load.

Reduced Disputes and Complaints

We’ve found that disputes often stem from inconsistent disclosures, poor documentation, or aggressive tactics. Automated debt collection software like Kompato AI eliminates that risk. Every interaction is logged, time-stamped, and delivered with regulatory precision.

With a 99.91% compliance pass rate, our platform ensures both transparency and peace of mind. As a result, we see significantly lower complaint rates, which supports brand reputation and reduces regulatory exposure.

Customer Relationship Preservation for First-Party Collectors

Collections isn’t always the end of a customer relationship, especially in fintech or banking. We recommend treating recovery as an opportunity to build long-term loyalty by offering borrowers flexibility, control, and respect throughout the process.

This is especially critical in first-party collections, where outcomes are often shaped in the first 90 days of delinquency. During this window, which can absorb a considerable amount of FTE effort, portfolios require tailored strategies. First-party cases frequently involve restructuring options or more complex scenarios like foreclosure or repossession. This makes a one-size-fits-all approach ineffective. Personalized and digital-first recovery flows are key to preserving both resolution rates and relationships.

Digital-first and empathetic experiences powered by debt collection automation software allow borrowers to resolve issues on their own terms.

Automation for Debt Collection Ensures Compliance Excellence

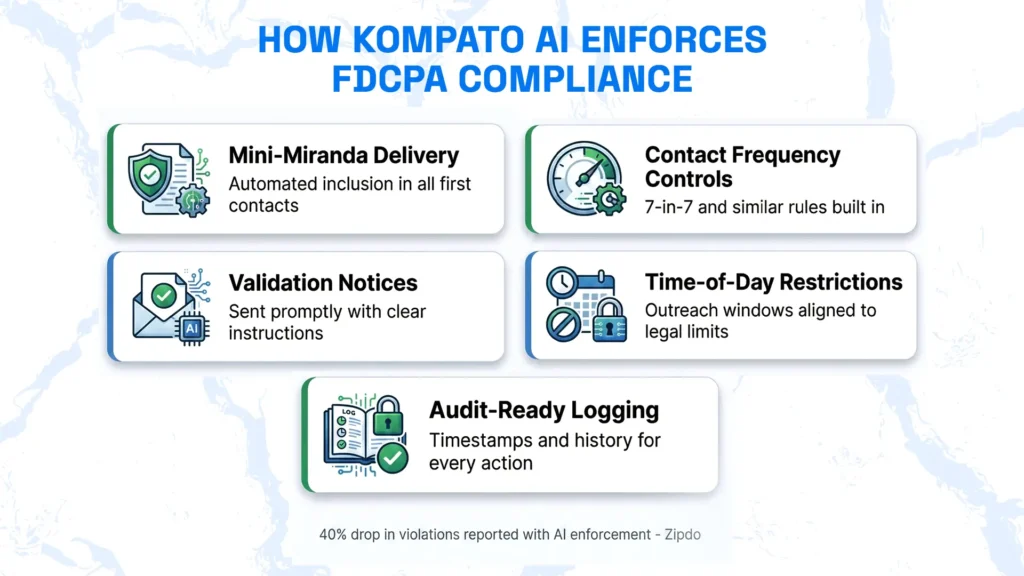

FDCPA Compliance Built Into Every Interaction

We’ve seen how manual oversight can create regulatory blind spots. Automated debt collection ensures that compliance is embedded in execution.

Disclosure language, communication windows, and contact frequency limits are hardcoded into Kompato AI’s logic. Whether it’s the mini-Miranda, a Model Validation Notice, or response windows under FDCPA, our system delivers every requirement at the right time.

According to Zipdo, AI tools have helped reduce compliance violations in debt collection by 40%.

TCPA and Contact Governance

TCPA compliance is one of the most misunderstood (and most litigated) areas in debt collection technology. Real-time consent tracking is critical.

Kompato AI automatically manages opt-ins, opt-outs, and channel-level consent changes using risk scoring and contact throttling logic. Dial attempts respect federally mandated hours and avoid restricted technologies or high-risk segments. Our platform ensures that governance is baked into daily operations and not dependent on agent memory.

Regulation F Requirements and Documentation

Regulation F is where we have seen many teams falter, especially around the 7-in-7 rule and cadence controls.

Kompato AI ensures these limitations are never breached. Messages are sequenced through automated debt collection software that respects both account status and communication history.

Every action, from validation notices to follow-ups, is logged with explainable AI (XAI) outputs. This lets you demonstrate why the system did what it did, which reduces audit overhead and eliminates downstream cleanups.

State-Specific Rules and Licensing Management

In the U.S., compliance isn’t federal-only. State-specific requirements can derail even the most well-intentioned recovery operation.

Kompato AI handles jurisdictional compliance at the account level. From adjusting message language to respecting contact-hour restrictions, the platform aligns with local laws. It even blocks outreach from unauthorized states, which ensures licensing violations never occur. This capability helps our clients scale nationally without adding legal risk.

It’s important to distinguish between collection and debt buying licenses. The latter involves separate requirements, with costs and processes varying widely by state. For companies expanding into new portfolios, these licenses can delay speed-to-market. Cost-saving measures may exist but require careful state-level review.

Kompato: The Complete AI-Powered Debt Collections Platform

Kompato AI is a full-stack debt recovery software platform built for the realities of modern recovery, like tight margins, rising oversight, and consumers who expect control and clarity. Our platform brings together AI, behavioral data, and automated orchestration to help lenders and debt buyers collect more, at lower cost, with full regulatory alignment. It is an operating system for digital-first collections.

Omnichannel AI That Treats Consumers with Respect

Kompato AI engages borrowers across SMS, email, voice, and portal in a coordinated and compliant manner with contextual memory. Every message is calibrated using predictive analytics and natural language processing (NLP) to reflect each consumer’s preferences, history, and risk profile.

Conversations feel personal because Kompato’s AI-driven debt collection technology adapts in real time. It respects context and reduces the fatigue caused by repetitive or irrelevant outreach.

Personalized Payment Portals with Dynamic Offers

Our self-service experience is far more than a static payment page. Borrowers see up-to-date balances, repayment plans, and settlement options that evolve based on their profile and past behavior.

Powered by conversational AI, the portal helps drive engagement and resolution, without the need for an agent. This makes Kompato AI a true automated debt collection software engine instead of a mere communication layer.

Compliance-by-Design Across Every Interaction

As seasoned recovery professionals, we’ve learned that true compliance is something you build into the foundation.

Kompato AI hard-codes FDCPA, TCPA, Regulation F, and state-specific licensing rules into every workflow. Risk scoring, consent governance, and audit-grade logs are all part of the platform’s DNA. This helps reduce legal exposure while making audits simple and clean.

Lower Costs with Stronger Recovery Economics

Our clients routinely see considerable reductions in cost per dollar collected, along with measurable improvements in liquidation rates, thanks to fewer manual escalations and smarter targeting.

Based on data from our deployments, Kompato AI autonomously resolves the vast majority of consumer interactions, requiring human escalation in fewer than 3.6% of cases. This shift away from manual workflows translates to major efficiency gains compared to traditional call centers, where agent intervention is often the default.

Instant Scalability Across Portfolio Sizes

Whether you’re managing 500 early-stage accounts or 500,000 charged-off loans, Kompato AI scales instantly, without adding agents or diluting performance.

The system flexes with your volume, so you don’t need to forecast headcount or retrain teams during portfolio shifts. This is collections technology that grows with your business.

Built for First-Party and Third-Party Portfolio Models

Kompato AI is designed for first-party and third-party recovery models. Lenders can run automated collections under their own brand, while debt buyers can standardize operations across acquired portfolios.

No matter the structure, you maintain full transparency and control.

Our Recommendations on Automated Collections: Final Thoughts

Automation is a structural shift in how recovery work gets done. Organizations that successfully automate debt collections will be those that treat compliance as architecture and consumer experience as a performance driver. The goal is not to replace people, but to free them from work that automated systems can now handle better.

We believe automation is most effective when it’s both operationally sound and ethically grounded. That’s the bar we’ve built Kompato AI to meet.

Whether you’re running first-party servicing or managing purchased portfolios, the fundamentals are the same: consistency matters, timing is essential, and trust is measurable. The systems we build today will define what responsible recovery looks like tomorrow.

Frequently Asked Questions

Automation typically cuts costs by 20-40% by reducing manual labor, improving agent efficiency, and minimizing compliance overhead.

Yes. Platforms use borrower history and behavior to guide real-time negotiations, routing complex cases with full context to human agents.

Leading systems embed FDCPA, TCPA, and Regulation F logic to ensure disclosures, timing, consent, and frequency rules are followed.

Simple setups take 4-6 weeks, while complex rollouts with custom workflows and integrations may take 12-16 weeks.

Automation avoids 20-50% agency commissions. Flat-fee platforms can cut operational costs by up to 40%.

Unsecured consumer debt, like credit cards, personal loans, BNPL, and early medical, sees strong outcomes, especially when data is fresh, and balances are moderate.

Respectful and well-timed outreach improves engagement. Borrowers often prefer self-service over live contact.

Automation can lift liquidation by 10-30%, especially in early-stage delinquency and well-segmented portfolios.

It removes manual errors like missed disclosures and contact violations, while providing a full audit trail.

Regulators favor systems that enhance borrower experience and follow the rules with documented audit trails.