The RMAI Annual Conference 2026 took place from February 9-12 at the Aria Resort & Casino in Las Vegas, bringing together debt buyers, originating creditors, collection agencies, law firms, compliance leaders, and technology providers from across the receivables ecosystem.

As the industry’s primary annual gathering, it serves as a working forum for operators and executives to exchange perspectives on regulation, performance, infrastructure, and risk.

This year’s conversations reflected an industry in the middle of structural change. Many institutions are actively replacing legacy infrastructure, moving core platforms from on-prem environments to cloud architecture, and reassessing how AI fits within regulated workflows. The discussion has shifted from proving that AI works to defining how it can be governed, approved, and embedded responsibly.

In this blog, we’ll share the key insights we heard at RMAI and explore how Kompato AI translates those pain points into practical, results-driven solutions for modern collections teams.

RMAI 2026 – What the Collections Industry Is Actually Thinking

If you listened closely to RMAI discussions, the message was clear:

The industry is rebuilding.

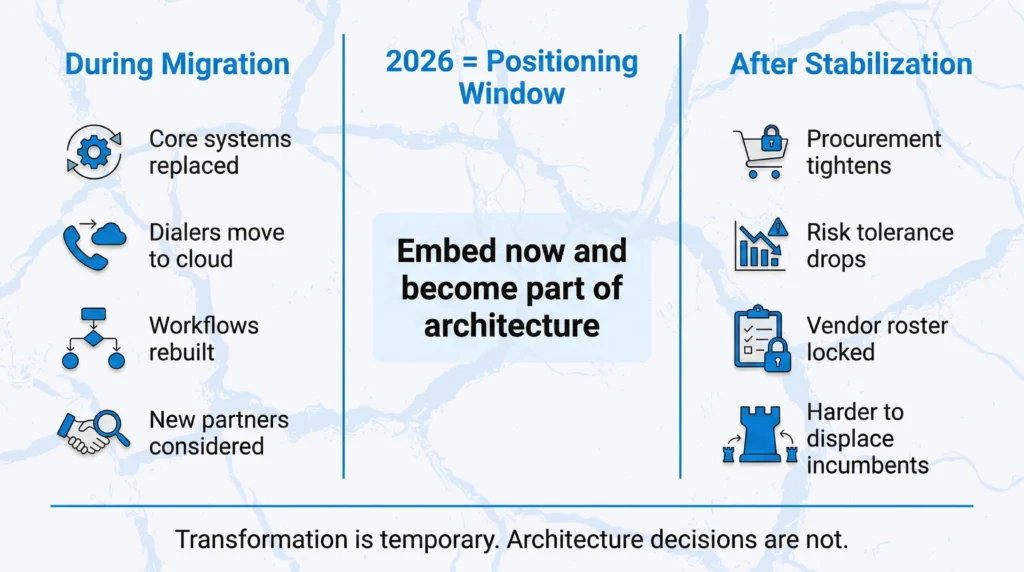

Across the industry, large issuers and servicers are navigating intensive migration cycles characterized by a wholesale replacement of core systems and the transition of dialers and workflow engines to cloud-native environments like AWS.

Some teams are deep into 18-month Pega migrations with tight controls on introducing anything new. Others are redesigning onboarding processes that have been customized for years and cannot be swapped out casually.

Collections remain in a transitional state, with the full scope of modernization still unfolding.

This is crucial because transformation windows are limited. Once systems stabilize, appetite for new structural partners drops.

Procurement tightens, and risk tolerance narrows. The focus shifts from building to protecting what was built.

Success in 2026 depends on aligning with and customizing each institution’s migration timeline.

Legacy Infrastructure Is Still Being Replaced

There is a perception that modernization is complete. On the ground, however, it is still underway.

Institutions described long migration timelines that restrict vendor intake. Dialer and contact infrastructure is being rebuilt, sometimes from scratch. Onboarding workflows remain tightly coupled to legacy systems, which makes change sensitive.

This is a high-stakes overhaul of a system currently in production. Embedding during migration means becoming part of the new architecture.

Waiting until after stabilization means entering an environment already optimized around others.

Missing the Transformation Window Means Starting Over

When a migration concludes, the organization has invested significant time and internal capital in the new stack. Stability becomes the priority at that point.

Introducing a new structural partner at that stage requires reopening governance reviews and absorbing fresh risk.

And buyers are not oblivious to this.

Vendors absent during migration are often evaluated as incremental additions rather than embedded operators, and that distinction influences procurement path and long-term relevance.

In that context, 2026 is a positioning year. The task is to align with transformation cycles before the window closes.

Governance Is the Gate – Not Skepticism

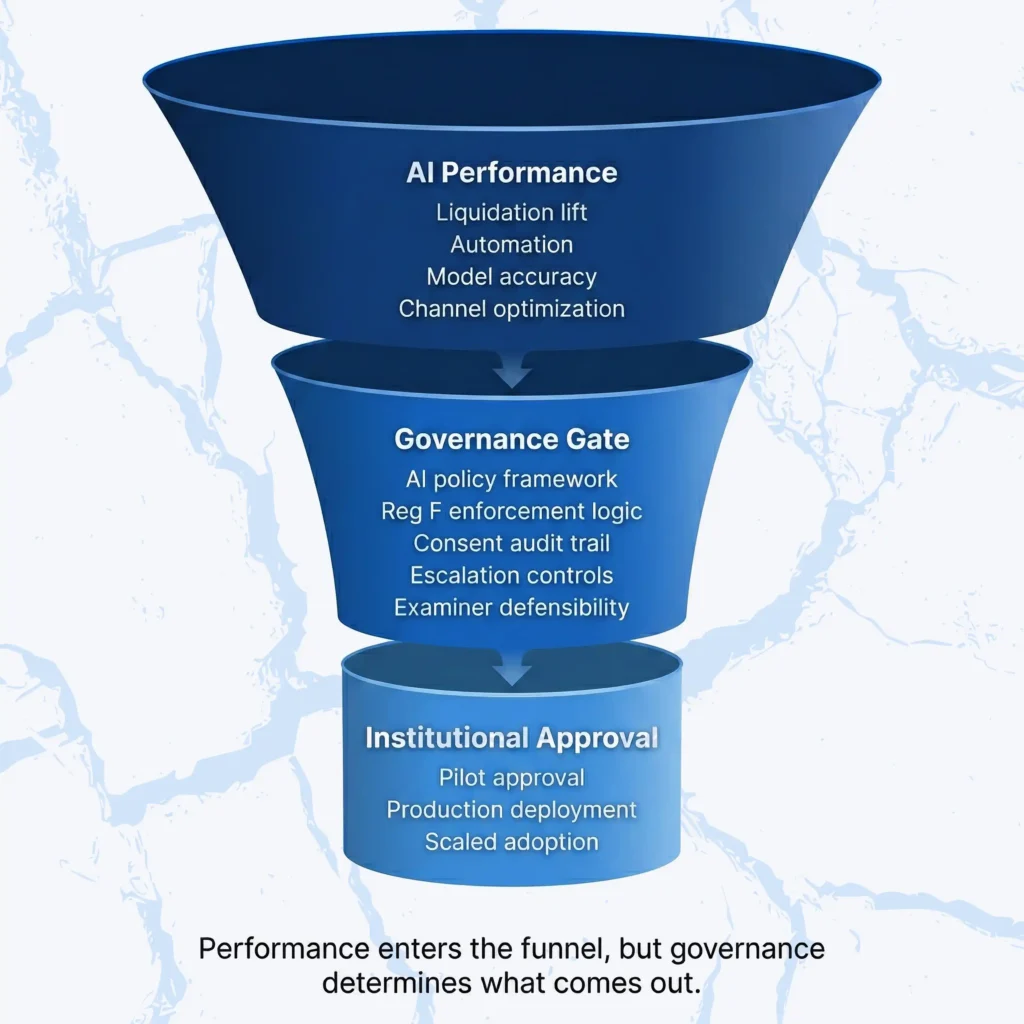

Compliance teams at RMAI expressed a willingness to adopt AI, provided the necessary structural safeguards are in place first.

Buyers largely assume AI can drive performance. What they do lack is a clear internal blueprint for approving it. Several compliance leaders said they expect comprehensive AI policy frameworks before anything scales, while others admitted they do not yet have a structured way to evaluate AI systems in regulated workflows.

This operational standstill stems from a missing architectural foundation: a clear governance roadmap. Without a mature governance framework to serve as the foundation, AI performance alone cannot unlock institutional adoption.

AI Exhaustion Is Real, But It’s a Governance Problem

Scott Hamilton’s framing of “AI exhaustion” resonated because the market does feel crowded. There are many vendors and many similar demos.

The deeper issue is that institutions often do not have mature AI governance frameworks. Compliance teams are asked to evaluate systems without a standardized rubric for escalation logic, monitoring, or audit traceability.

Every potential integration carries a heavy burden of scrutiny due to the lack of a stable underlying framework. The fatigue comes from structural uncertainty.

The Question Buyers Are Really Asking

Private discussions centered almost exclusively on an architecture’s ability to withstand a rigorous examination.

Buyers want to understand how Reg F is enforced, how consent is captured and logged, how escalation logic is defined, and how scripts remain consistent. They are listening for clarity.

And this demand for clarity highlights the importance of language. Describing systems as enforcing predefined rules and operating within guardrails builds confidence. In regulated environments, governance architecture carries more weight than incremental liquidation gains.

If compliance cannot explain the system clearly to an examiner, the deployment will not proceed.

Cost Pressure Is the Budget Driver – Not Innovation

Cost pressure was one of the clearest themes at RMAI, and it is being measured precisely.

One institution described a nine-figure operational cost mandate shaping every investment decision. Others emphasized close tracking of cost per dollar collected. Headcount reductions have already taken place in parts of the industry, with teams moving toward leaner digital-first models.

We are witnessing a definitive evolution of the core system structures.

In this context, innovative language carries less weight than operating economics. Digital strategies are evaluated for their impact on complaint rates, staffing glide paths, and long-term cost-to-income ratios. Consistency reduces variance, and lower variance reduces supervisory overhead. Those changes show up directly in efficiency metrics.

Performance claims still open the door. However, the conversation doesn’t take long to turn to cost structure. Finance and operations leaders want to understand how technology reshapes the expense base over time.

In 2026, AI is positioned most effectively as an operating infrastructure that improves efficiency while maintaining compliance clarity. Performance draws interest, but structural cost improvement is what secures the budget.

AI Agency vs. AI Vendor – A Distinction That Changes Everything

One question came up repeatedly at RMAI: Are you a vendor, or are you an agency?

And it was not a casual question. It was an inquiry about category, and category is what determines procurement path, risk allocation, and long-term relevance.

Vendors are evaluated as technology overlays. They sit alongside existing operators and move through IT reviews, contained pilots, and performance comparisons.

Agencies, on the other hand, assume operational responsibility. They sit inside the collections process itself, and the discussion shifts to servicing standards, liability, and governance architecture.

This distinction redefines the strategic landscape. If you are seen as a vendor, you enter a crowded evaluation lane. If you are understood as a licensed operator, the discussion moves to operating model design and structural partnership.

This is where Kompato’s positioning is clear: Kompato is the first nationally licensed AI collection agency. This model represents a native fusion of AI and operational logic, where the system itself executes the process through a framework of embedded compliance and digital cycles.

In first-party contexts that may resemble a vendor framework. In third-party environments, it functions as a licensed servicer. The structure adapts, but the operating model remains consistent.

Buyers are prioritizing the ethical and operational integrity of the system. Clarity on whether you are a tool or an operator determines if you are tested as an add-on or embedded as infrastructure.

Controlled Pilots Are the Real Path to Scale

There was little debate at RMAI about whether AI belongs in collections. The hesitation is institutional risk management.

Large organizations move through staged approvals. Internal champions need safe entry points that allow learning without exposing core portfolios to volatility.

Buyers described starting with aged inventory, warehouse accounts, digital-only channels, or tertiary placements before expanding into primary volume.

This sequencing reflects governance reality. Early wins must be defensible, and risk must be contained before broader adoption.

Vendors often push for immediate scale, while buyers move in phases.

Kompato’s deployment model follows that logic. It begins where risk tolerance is highest and expands as governance comfort grows. The objective is to demonstrate performance and compliance in a defined segment, then extend from there.

Scale is earned through a series of successfully cleared trust milestones.

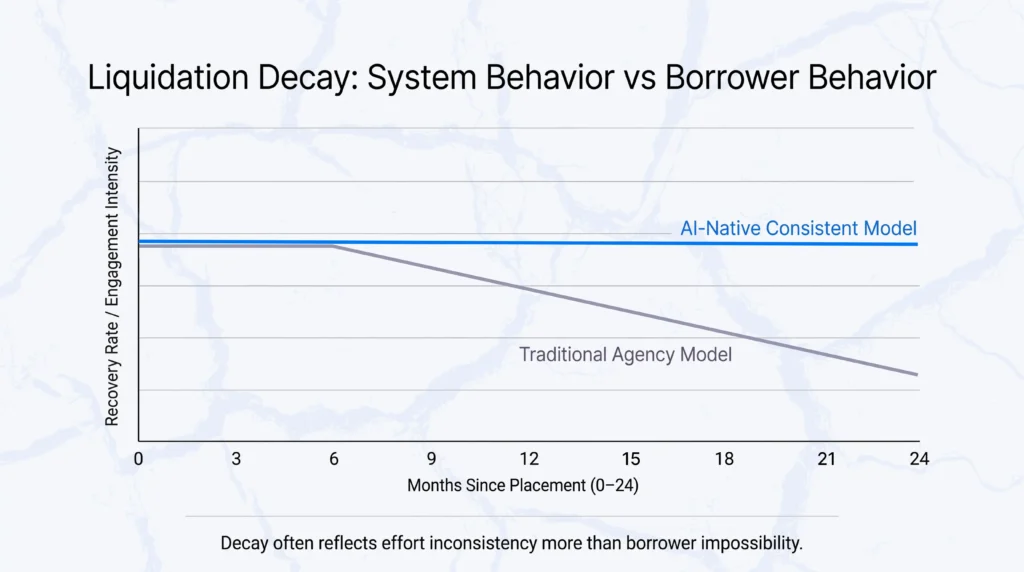

The Myth of Liquidation Decay

Aging inventory was discussed candidly at RMAI.

Traditional agency models often deprioritize accounts after six to ten months. Attention shifts to newer placements, outreach becomes less consistent, and performance declines. This drop is often attributed to borrower exhaustion.

Several buyers questioned that assumption. They are asking for sustained engagement over 18 to 24 months, recognizing that what appears to be borrower impossibility may actually be operational fatigue.

Human-driven systems experience effort decay, as priorities shift and consistency erodes. That is not the case with AI, though: it maintains cadence, logic, and follow-through across the life of an account.

This systemic consistency stabilizes long-tail recovery curves. AI-native operators can extend recovery curves because engagement does not taper off. Kompato’s model leverages this concept to extract value from older accounts through a relentless automated cadence.

Decay should not be treated as a natural ceiling. In many cases, it reflects how the system behaves instead of how the borrower does.

What 2026 Is Really About

The themes at RMAI point in a clear direction: the industry is mid-transformation.

As governance frameworks take shape and budget constraints intensify, organizations are adopting a more deliberate approach to pilot programs while simultaneously looking toward aging inventory for untapped value.

These signs are reflective of a market that is deciding how AI should be embedded.

That is why 2026 is a positioning year.

Institutions embedding AI during active migration cycles are reshaping their operating model for years ahead. Once systems stabilize, introducing new structural partners becomes harder, and governance tightens.

The language of “selling AI tools” no longer fits this moment. The opportunity is to become part of the operating model itself.

For Kompato, the conversations reinforced this path. The focus is on building an AI-native collections infrastructure that fits inside regulated environments with clear licensing, compliance enforcement, and a sustained recovery strategy.

Those who align with institutional transformation cycles now will carry a structural advantage into 2027 and beyond.

Final Thoughts on RMAI 2026

The true value of RMAI this year was in candid discussions regarding migration timelines, governance gaps, and the fiscal mandates shaping the industry.

We are grateful for those discussions and the clarity they brought. Kompato will continue sharing direct observations from the field as the market evolves.

If any of this reflects what your team is navigating right now, we would welcome the conversation.